Chargeback Prevention for Free Trials, The Settings That Reduce “I Forgot” Disputes

Feb 03, 2026

Free trials are supposed to feel risk-free. For customers, that often turns into “I didn’t know I’d be charged.” For merchants, it turns into free trial chargeback prevention work that eats time, revenue, and trust.

The tricky part is that many “I forgot” disputes aren’t true fraud. They’re friction. A customer didn’t notice the end date, didn’t see the price again, couldn’t find the cancel link, or didn’t recognize the billing descriptor on their card statement.

This post breaks down the exact trial and billing settings that reduce those disputes, without killing conversion.

Why “I forgot” disputes spike with free trials

A free trial is like borrowing a book from a friend. If nobody agrees on the return date, someone gets annoyed later. Trials work the same way, especially when the first paid charge happens silently.

Recent industry reporting (2024 to 2025) suggests subscription businesses often sit around 0.5% to 1% chargeback rate on transactions, and “friendly fraud” makes up a large share of disputes. Free trials are a common trigger because the customer’s story sounds believable: “I never used it,” “I canceled,” “I forgot.”

Even if your terms are technically clear, card networks and issuers look at customer experience signals. If the billing looks confusing, or cancellation is hard, the issuer may side with the cardholder.

“I forgot” disputes usually come from a small set of root causes:

- End date isn’t memorable: The customer saw it once, then life happened.

- Price isn’t repeated near the decision: They remember “free,” not “$29 next week.”

- Billing descriptor looks unfamiliar: “CHGBS*XYZ” doesn’t match your product name.

- Cancellation is hidden: People dispute when they feel trapped.

- Confirmation is weak: No receipt, no reminder, no paper trail.

If you fix those, you prevent a big chunk of avoidable disputes.

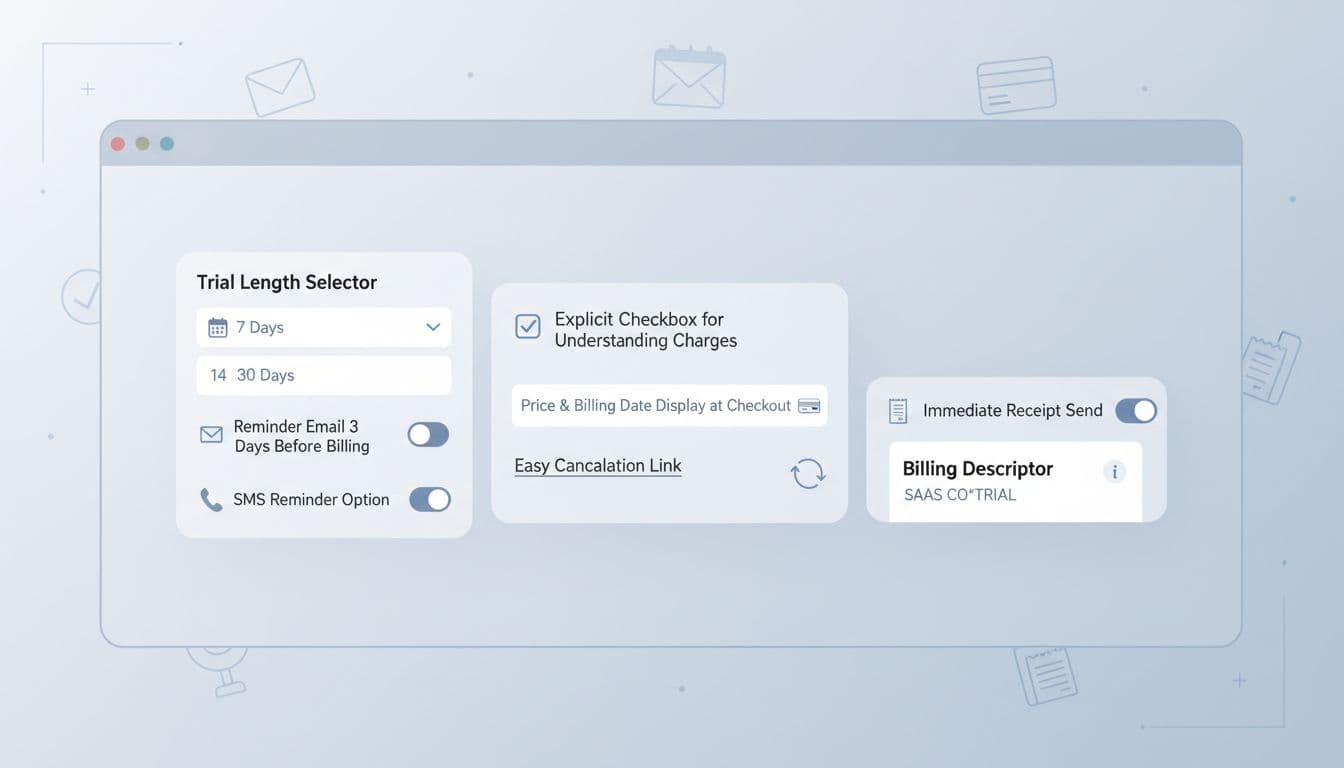

The free trial settings that reduce “I forgot” chargebacks

Think of these settings as “memory anchors.” Each one creates a moment where the customer re-learns the billing facts before the first charge.

Here’s the short list that tends to move the needle fastest:

| Setting | What the customer experiences | Why it cuts “I forgot” disputes |

|---|---|---|

| Show price + billing date at signup | “Free for 7 days, then $X on Jan 30” | Removes the “surprise charge” feeling |

| Require an explicit checkbox | “I understand I’ll be charged after trial” | Creates clear consent and evidence |

| Send multi-step reminders | Email (and optional SMS) before billing | Gives time to cancel before frustration |

| Add an easy cancellation link | One-click path to cancel from messages | Prevents disputes caused by “can’t cancel” |

| Send an instant receipt/confirmation | A timestamped email right after signup | Stops “I never signed up” narratives |

| Preview the billing descriptor | “This charge will appear as…” | Reduces “I don’t recognize this” disputes |

A few implementation details matter more than people expect:

1) Reminder timing beats reminder volume.

One reminder is better than none, but three tends to be the sweet spot for first-charge clarity: 7 days, 3 days, and 1 day before billing (adjust based on trial length). The message should repeat the same facts every time: product name, price, billing date, and cancel path.

2) Put the cancel link where emotions are.

Customers look for it when they get a reminder or see an unexpected charge. Add the cancellation link inside the reminder and the receipt, not just in a settings page.

3) Be consistent across checkout, email, and account.

If your checkout says “Pro Plan,” but your emails say “Premium,” disputes rise. Consistency helps customers recognize what they bought later.

If you’re using a hosted checkout or billing tool, configure trials so those details show up clearly during purchase. Stripe’s guide on configuring free trials in Checkout is a solid reference for what’s possible at the payment layer.

Billing descriptors and recurring rules: small changes, big dispute impact

Most “I forgot” disputes happen days or weeks after signup. By then, the only thing the customer sees is their bank app. That’s why billing descriptors and recurring payment practices matter.

Start with descriptor hygiene:

Use a descriptor customers recognize. Aim for your brand name or product name (within processor limits). If you must use an abbreviation, match what customers saw at signup.

Add a support-friendly phone or URL (when supported). Some processors allow dynamic descriptors or extra fields. When a customer can contact you quickly, they’re less likely to file a dispute first.

Also review how your recurring billing aligns with card network expectations for subscription transparency. If you want a practical overview of what networks look for, this explainer on Visa recurring payments guidelines helps frame the common pitfalls (like unclear terms, cancel friction, and descriptor confusion).

Two more settings that help with “I forgot” cases:

Grace period for first charge: If someone complains within 24 to 48 hours of the first billing, consider an automatic refund policy. Many “I forgot” disputes happen because the customer panics. A fast refund is often cheaper than a chargeback fee plus operational time.

Immediate post-charge receipt: Send a receipt the moment the first paid invoice hits. Include: what was charged, what plan, the service period, and the cancel link.

For broader reduction practices across dispute types, Stripe’s overview of ways to reduce chargebacks is a useful checklist.

Making free trial chargeback prevention scalable with Chargebase

Settings reduce disputes, but high-volume teams still get stuck playing whack-a-mole. Issuer alerts and automated resolution are what make prevention sustainable.

Chargebase is a chargeback prevention and recovery platform for e-commerce and SaaS businesses. It connects to your payment provider quickly, then uses global merchant data plus network programs like Verifi’s CDRN and RDR, along with Ethoca alerts, to spot disputes early and help stop them before they become chargebacks.

A few practical reasons teams use Chargebase for free-trial-heavy funnels:

- Real-time alerts when they matter: You get notified when an alert can actually prevent a chargeback, so your team isn’t drowning in noise.

- Automation rules for outcomes: With RDR, you can apply 10+ rules to decide when refunds happen automatically, which is ideal for “I forgot” scenarios where fighting the dispute rarely pays.

- Performance-based pricing: Pricing is pay-per-alert, which keeps costs tied to results. Chargebase lists pricing such as $15 per alert for CDRN and RDR, and $25 per alert for Ethoca, so forecasting is straightforward.

- Lower ops load: Automating the full dispute cycle means fewer manual tickets, fewer rush refunds, and fewer “please cancel me” threads that turn into bank claims.

If your trials are growing, the goal isn’t just fewer chargebacks. It’s fewer chargebacks with less work.

Conclusion

“I forgot” disputes are a customer memory problem, not a mystery. When you repeat the billing facts, make cancellation easy, and keep descriptors recognizable, free trial chargeback prevention becomes mostly a settings exercise.

Start by tightening disclosure, reminders, and cancellation placement, then add alert-based automation if volume is high. The best outcome is boring: customers know what’s coming, and chargebacks don’t show up at all.

You might also want to read

Uncategorized

Jun 07, 2026

Uncategorized

Jun 06, 2026

Manual vs. Automated Processes

Jun 05, 2026

Uncategorized

Jun 04, 2026