Chargeback Lifecycle Explained (2026), from First Dispute to Pre-Arb (With a Simple Timeline)

Feb 06, 2026

A chargeback can feel like a surprise bill that shows up weeks after the cardholder already left angry. One day, a sale looks settled. The next, the money is pulled back, you get hit with fees, and your team is digging through emails and logs.

Understanding the chargeback lifecycle is the foundation of effective chargeback management, how you stop treating disputes like random lightning strikes. When you know the stages and the clock at each step, you can decide when to refund, when to fight, and when to prevent the whole thing before it becomes a formal chargeback.

This guide walks through each phase, from the first cardholder complaint all the way to pre-arbitration (pre-arb), with a simple timeline you can share internally.

The chargeback lifecycle in 2026, who’s involved and why timing hurts

A chargeback is not just “customer vs merchant.” It’s a chain that runs through several parties:

- Cardholder: the customer who disputes.

- Issuing bank: the customer’s bank.

- Acquiring bank: your bank or acquiring partner.

- Card network: Visa, Mastercard, Amex, Discover set the rails and rules.

- Merchant: you, plus your PSP, gateway, and tools.

In 2026, prevention matters more because chargebacks are expensive even when you “win.” Industry reporting still commonly cites that the all-in cost can be multiple times the disputed amount (one recent estimate pegs it at about $3.75 per $1 disputed). On top of direct chargeback fees and lost goods (especially from card-not-present fraud), chargebacks also impact your chargeback ratio, and that can trigger risk reviews from processors.

Networks also keep pressure on thresholds. Recent merchant guidance commonly references targets around 0.65% for Visa and 1% for Mastercard, because crossing limits can put your merchant account at risk of monitoring programs and penalties. If you want practical ways to keep ratios down, Chargebase’s doc on strategies for lowering chargeback ratios breaks it into simple operational steps.

The other big issue is time. Cardholders often have up to 120 days to file certain disputes (with some categories shorter), and a retrieval request might precede a formal dispute, but merchants rarely get anything close to that to respond. Network rules may allow 20 days per stage for Visa, Discover, and Amex, and longer windows for Mastercard phases, but your acquiring bank often sets a shorter response deadline for dispute resolution. In real operations, many teams feel like they have 5 to 10 days to build a response before it’s too late.

That’s why alerts and “pre-dispute” programs exist: they move the work earlier, when the outcome is still flexible.

For a broader merchant-friendly primer, see this chargeback management guide (2026).

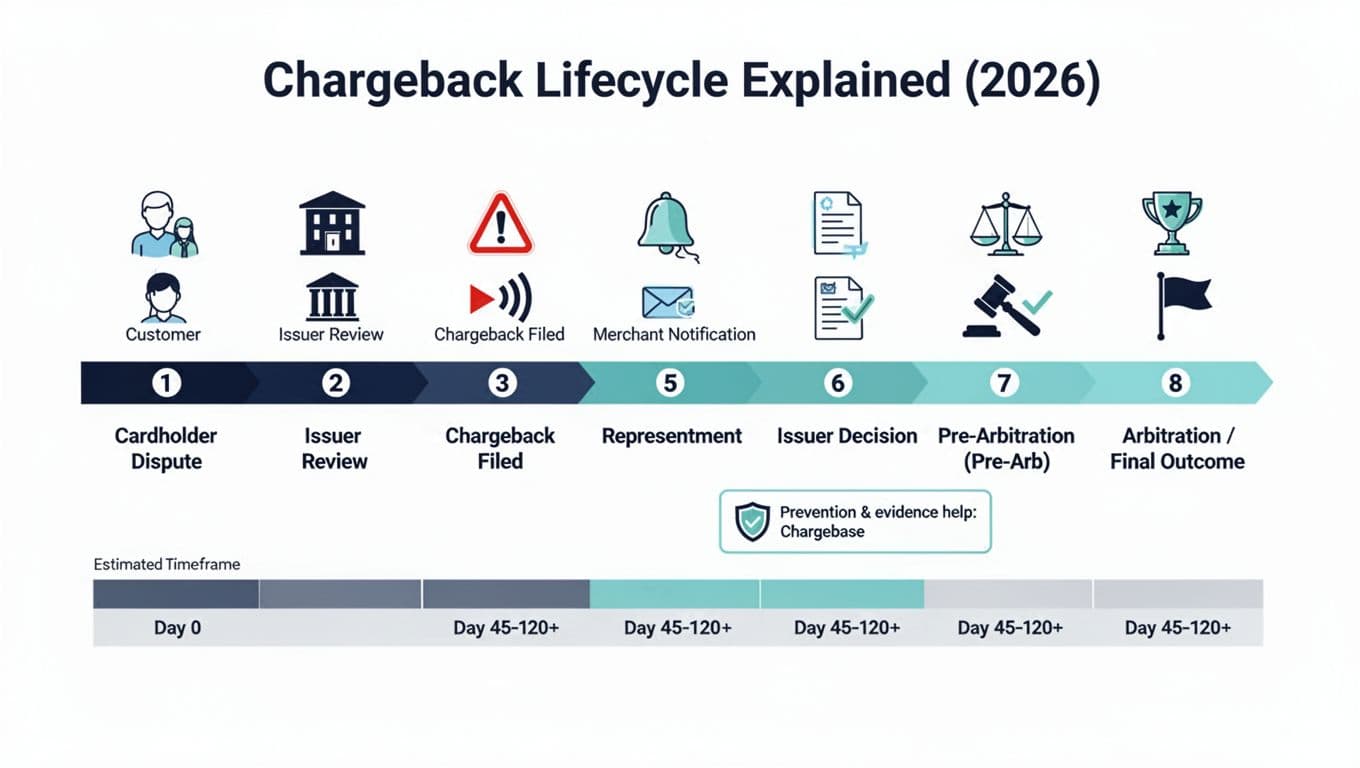

Chargeback lifecycle timeline chart (dispute to pre-arb, step by step)

The chargeback lifecycle begins after the first presentment, when the transaction is initially processed through the card network before any dispute arises. Different networks and reason codes shift the exact dates, but the flow below is reliable enough to train teams and set expectations.

Simple timeline chart (typical ranges)

| Stage | What happens | What the merchant should do | Typical timing (rough) |

|---|---|---|---|

| 1) Cardholder dispute | Cardholder initiates dispute in their banking app or by calling the issuer | Try to intercept via support and clear comms, watch for alerts | Day 0 |

| 2) Issuer review | Issuing bank reviews claim and transaction data; may provide provisional credit to the customer | If you get an alert, decide fast: refund or hold | Day 0 to Day 2 |

| 3) Chargeback filed | Issuing bank initiates chargeback through the network (e.g., Visa Resolve Online or Mastercom) | Prepare evidence plan, identify root cause | Day 2 to Day 30+ |

| 4) Merchant notification | Acquiring bank/PSP notifies merchant and debits funds temporarily | Triage, assign owner, check internal deadlines | Often within days of filing |

| 5) Representment | Submit compelling evidence to contest | Send clean, complete evidence package | Often due in 5 to 20 days (sometimes more) |

| 6) Issuer decision | Issuer accepts or rejects your representment | If rejected, evaluate pre-arb economics | Day 20 to Day 60+ |

| 7) Pre-arbitration (pre-arb) | One side challenges again (may involve second presentment or second chargeback attempt), trying to settle before arbitration | Negotiate or concede if odds are poor | Day 45 to Day 120+ |

| 8) Arbitration process / final outcome | Network decides final result, fees increase | Reserve for high-value, high-confidence cases | Can extend beyond 120 days |

What “pre-arb” really means

Pre-arb is the stage most merchants only learn about after they lose representment. Think of it as the “last serious conversation” before the networks become the judge. If the issuing bank rejects your representment, the case can escalate into pre-arb, where the parties exchange positions again. The reason code assigned to the case determines the specific rules for the arbitration process and how the issuing bank evaluates the rebuttal. Fees and effort rise, and the business decision becomes sharper: is this worth continuing, or should you cut losses and fix the root cause?

If you want another perspective on the stages (and the terms people use differently), this guide to the chargeback life cycle is a helpful reference.

Where merchants win or lose: prevention windows, evidence quality, and Chargebase automation

Most teams focus on representment because it feels like the “official” fight. The real money, time, and stress savings usually come earlier, before a dispute becomes a network chargeback.

The prevention window is short, but powerful

When a customer complains to their bank, you may have only 24 to 72 hours in some alert programs to stop the chargeback by issuing a refund. That’s not much time, but it’s often enough if your process is ready.

This is where Chargebase fits. Chargebase is chargeback prevention software for e-commerce and SaaS companies. It connects to your payment provider with a no-code setup (often just minutes), then uses dispute-prevention networks and flows like Ethoca, Verifi CDRN, and Rapid Dispute Resolution to detect disputes early and help you prevent chargebacks before they hit your ratio.

A few practical traits stand out for ops teams:

- Real-time alerts only when they matter: the goal is actionability, not noise.

- Performance-based pricing: you pay per alert, not a big fixed contract.

- Automation options: for example, Rapid Dispute Resolution can support rules-based auto-refunds to stop friendly fraud before it impacts your merchant account, and Chargebase supports 10+ automation rules so you can decide what gets refunded automatically versus reviewed.

If you’re evaluating the Mastercard side specifically, Chargebase’s explanation of what is Ethoca for chargeback prevention is a clear starting point.

Evidence wins cases, but only if it’s tight

When you do contest a chargeback, evidence has to be easy for the issuer to accept quickly. Compelling Evidence 3.0 is the new standard for fighting disputes, where the basics still matter in 2026:

A clean packet usually includes proof of delivery or service use, order details, billing descriptor clarity, customer communication, refund policy acceptance, login or IP history for digital goods, and any cancellation record for subscriptions. Tight evidence documentation like this boosts your win rate. Missing one key piece often sinks the whole response.

A simple rule for your team

Treat disputes like a kitchen fire. If you catch smoke early, you turn off the heat (refund, cancel shipment, fix confusion). If the fire reaches the walls (chargeback filed), you’re now dealing with paperwork, chargeback fees, and damage control. Checking the specific reason code is crucial to tailor your response.

For more on how the fight itself has changed this year, see How to Fight Chargebacks in 2026.

Conclusion

The fastest way to lower losses through effective chargeback management isn’t winning more representments. It’s shortening the path from “issuer hears a complaint” to “merchant takes action.” Once you map your chargeback lifecycle from dispute to pre-arb, you can build clear rules for refunds, evidence, and escalation, and you can plug in alerts so fewer cases ever become chargebacks, leading to smoother dispute resolution.

If chargebacks feel unpredictable today, take one week and track where your last 20 disputes really started, with a focus on cardholder behavior and friendly fraud. The patterns usually show up fast.

You might also want to read

Uncategorized

Jun 07, 2026

Uncategorized

Jun 06, 2026

Manual vs. Automated Processes

Jun 05, 2026

Uncategorized

Jun 04, 2026