Friendly Fraud in 2026: Common Patterns and How to Stop Them

Feb 08, 2026

If chargebacks feel like a leak you can’t fully patch, there’s a reason. In 2026, friendly fraud, also known as first-party misuse, sits behind most disputes for many e-commerce and SaaS brands, and it often doesn’t look like “fraud” at all. Unlike chargeback fraud driven by malicious strangers, friendly fraud involves real customers with varying levels of intentionality.

It’s the real customer, using a real card, enjoying frictionless shopping for a real purchase, then disputing it. Sometimes it’s deliberate. Other times it’s confusion, a forgotten renewal, or a kid buying add-ons on a parent’s phone. Either way, you lose time, fees, product, and momentum.

The good news is that friendly fraud follows repeatable patterns. Once you map those patterns, you can block a big chunk of them before they become chargebacks.

Why friendly fraud keeps winning in 2026

Friendly fraud is simple: the cardholder (or someone in their household) makes the purchase, then later tells the bank “I didn’t do this” or “I didn’t get what I paid for,” or claims Not Sufficient Funds (NSF) as a secondary reason to recoup funds. With more shopping, more subscriptions, and more one-tap payments, disputes have become the shortcut some customers take instead of contacting support.

An e-commerce fraud survey in the last couple of years regularly describes friendly fraud as the majority of chargebacks, often estimated in the 70 to 80 percent range across many online categories. Even if your mix is lower, it only takes a small jump to push your chargeback ratio into the danger zone (higher fees, stricter processing terms, and more internal workload). For a current merchant-oriented view, see the 2026 merchant chargeback handbook.

Two environmental shifts in 2026 make disputes harder to manage than before, even with evolving AI fraud detection systems that flag high-risk transactions:

First, bank apps make disputes feel like a normal support channel. A customer can tap “dispute transaction” while standing in line for coffee.

Second, product journeys are easier to misuse. If your cancellation flow is hard to find, if your shipping updates are vague, or if your descriptor is confusing on credit card statements, customers interpret that friction as “the merchant won’t help.” A thoughtful product lens on this is described in fraud as a misuse case.

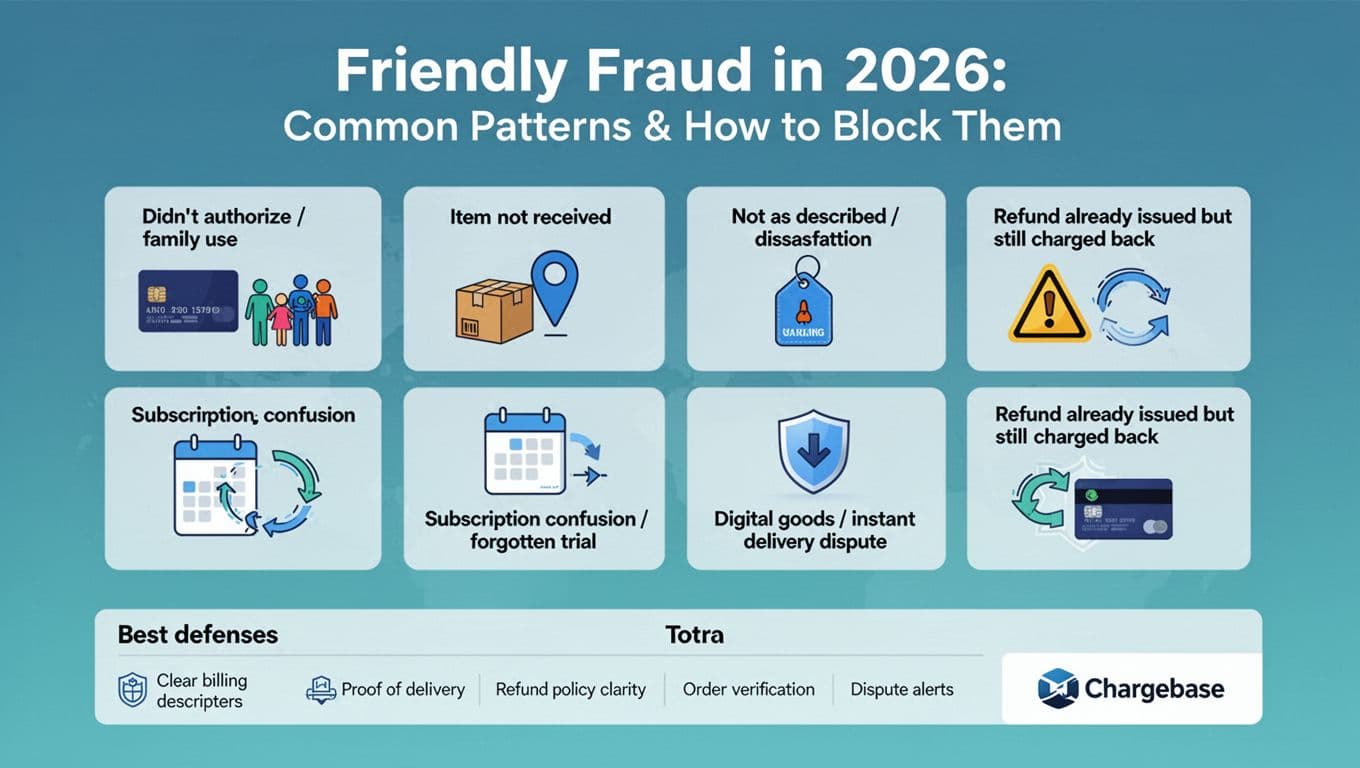

Friendly Fraud in 2026, the most common patterns (and how to block each one)

Friendly fraud usually shows up in a handful of repeat complaints tied to specific customer behavior patterns. Treat each one like a playbook, not a mystery. Here’s the quick map, then the “block it” detail right after.

| Pattern customers claim | What’s usually happening | Best way to block it |

|---|---|---|

| “I didn’t authorize this” | Family use, impulse buys, or buyer’s remorse reframed as fraud | Clear billing descriptors, strong identity verification, fast lookup and support |

| “Item not received” | Delivery confusion, porch theft claims, or false non-delivery | High-quality tracking, delivery confirmation, shipping expectation emails |

| “Not as described” | Buyer disappointment, unclear listings, poor fit expectations | Better product pages, photo accuracy, easy returns and exchanges |

| “I canceled” (subscription) | Forgotten trial, unclear cancel steps, renewal surprise | Subscription reminders, simple cancel, “what happens next” emails |

| “Digital goods not delivered” | Instant delivery ignored, account sharing, chargeback after use | Delivery logs, access logs, digital receipts, abuse controls |

| “I already got a refund” | Duplicate refunds, slow processing, refund to different method | Refund policy checks, reconciliation, clear refund timelines |

Now, the “how to block it” detail, written for teams that actually have to execute it:

“I didn’t authorize this” (family use, or post-purchase regret).

This one spikes when the billing descriptors don’t match your brand, or when the buyer used Apple Pay, a virtual card, or a partner checkout and forgets. Tighten your billing descriptors, and send a clean receipt that repeats the same name. For higher-risk orders, step up identity verification with AVS, CVV, 3D Secure 2.0, device intelligence, and behavioral biometrics where it fits. Don’t bury support either; when customers can’t reach you, the bank becomes support.

“Item not received” after tracking shows delivery.

A lot of these are real confusion (wrong door, mailroom, carrier scan timing). Some are abuse linked to customer behavior patterns. Your best defense is boring and consistent: accurate tracking links, delivery confirmation, and proactive “out for delivery” updates. For high-value items, consider signature on delivery or pickup verification. If you ship in multiple boxes, say so early, because partial shipments create disputes.

“Not as described” (dissatisfaction disputes).

This is buyer’s remorse wearing a nicer outfit. It tends to happen when photos are over-edited, sizing is vague, or key limitations are hidden in FAQs. Fix the product page first, then the refund policy. A clear return path reduces the urge to dispute. If you sell SaaS, translate features into outcomes, and show what’s included on each plan inside the app, not only on the pricing page.

Subscription confusion (forgotten trial, renewal surprise, “I canceled”).

This is where tiny UX decisions turn into chargebacks. Put the renewal date and amount in the welcome email with subscription reminders, and again a few days before billing. After a cancellation, send a confirmation that states what access remains and until when. If you want practical ideas that merchants use right now, this friendly fraud prevention guide lays out common friction points to fix.

Digital goods and instant delivery disputes.

When delivery is instant, customers sometimes argue “nothing arrived,” even though access was granted. Capture delivery evidence that a human can understand later: timestamped access logs, download events, license key views, and digital receipts. Also watch for account sharing, unusual login patterns, and repeat customer behavior patterns, because “friendly fraud” and account misuse overlap in digital products.

“Refund already issued” but the chargeback still lands.

This is often operations, not fraud: a refund processed late, a refund to a different tender, or a second refund accidentally triggered. Add a hard check that blocks a second refund on the same transaction unless a manager approves it. Spell out refund policy timelines in the confirmation email, including that banks can take days to post it.

Stopping friendly fraud before it becomes a chargeback (where Chargebase helps)

Winning chargebacks via the representment process after the fact is expensive, and the merchant win rate is not great if you are missing Compelling Evidence 3.0 or submitting late. The real advantage comes from acting earlier, while the issue is still a pre-dispute.

That is where chargeback alerts and rules-based resolution help. Chargebase, a leader in automated dispute solutions built for e-commerce and SaaS teams, connects to your payment provider with a no-code setup (often in about 2 minutes). It then uses networks and programs like Ethoca, Verifi’s Cardholder Dispute Resolution Network (CDRN), and Rapid Dispute Resolution (RDR) to surface chargeback alerts early. These chargeback alerts facilitate communication with the card issuer before a formal dispute is filed, so you can stop them and build an evidence trail with captured logs, including multi-factor authentication data.

Two practical details matter when you are planning workload:

- Real-time alerts only when useful, so you are not paying for noise.

- Performance-based pricing, where you pay per alert (examples from common alert programs include about $25 per Ethoca alert, and around $15 per CDRN or RDR alert), so the cost stays tied to actual prevention.

Chargebase also supports automation. With RDR, you can set dispute rules and auto-resolve eligible cases (often via auto-refund), which helps when response windows are tight and weekends happen. If you want the bigger picture on keeping ratios under control, Chargebase’s docs on best practices for low chargeback rates break down what to track (acceptance rate, time to action, and avoiding double refunds). For a deeper explainer on alert networks, this guide on Ethoca alerts for chargeback prevention gives a clear “how it works” view.

Conclusion

Friendly fraud doesn’t stop because you write better rebuttals. It slows down when you remove confusion, prove delivery and usage, and act early when a dispute signal appears. The patterns in 2026 are consistent, which means your defenses can be consistent too.

If you treat chargeback fraud like a system problem (not a customer-by-customer argument), you’ll prevent more chargebacks, protect your ratios, and spend less time chasing paperwork. The fastest wins usually come from early chargeback alerts, order confirmation emails, blocked lists to stop repeat offenders, clear billing, and simple customer paths that make support easier than disputing. These steps safeguard your merchant’s bottom line.

You might also want to read

Uncategorized

Jun 07, 2026

Uncategorized

Jun 06, 2026

Manual vs. Automated Processes

Jun 05, 2026

Uncategorized

Jun 04, 2026