3D Secure Liability Shift Explained for Ecommerce and SaaS in 2026

Mar 18, 2026

A chargeback can feel like getting billed twice. You lose the sale, then you lose time and margin cleaning up the mess. That’s why 3D Secure liability shift matters so much in 2026.

Here’s the short version: when 3D Secure authentication succeeds, fraud liability often moves from the merchant to the card issuer. However, that protection has limits. It helps with fraud disputes, not every dispute, and SaaS renewals often sit outside the safe zone. If you accept card payments online, knowing where the shift starts and stops can save real money.

What 3D Secure liability shift really covers

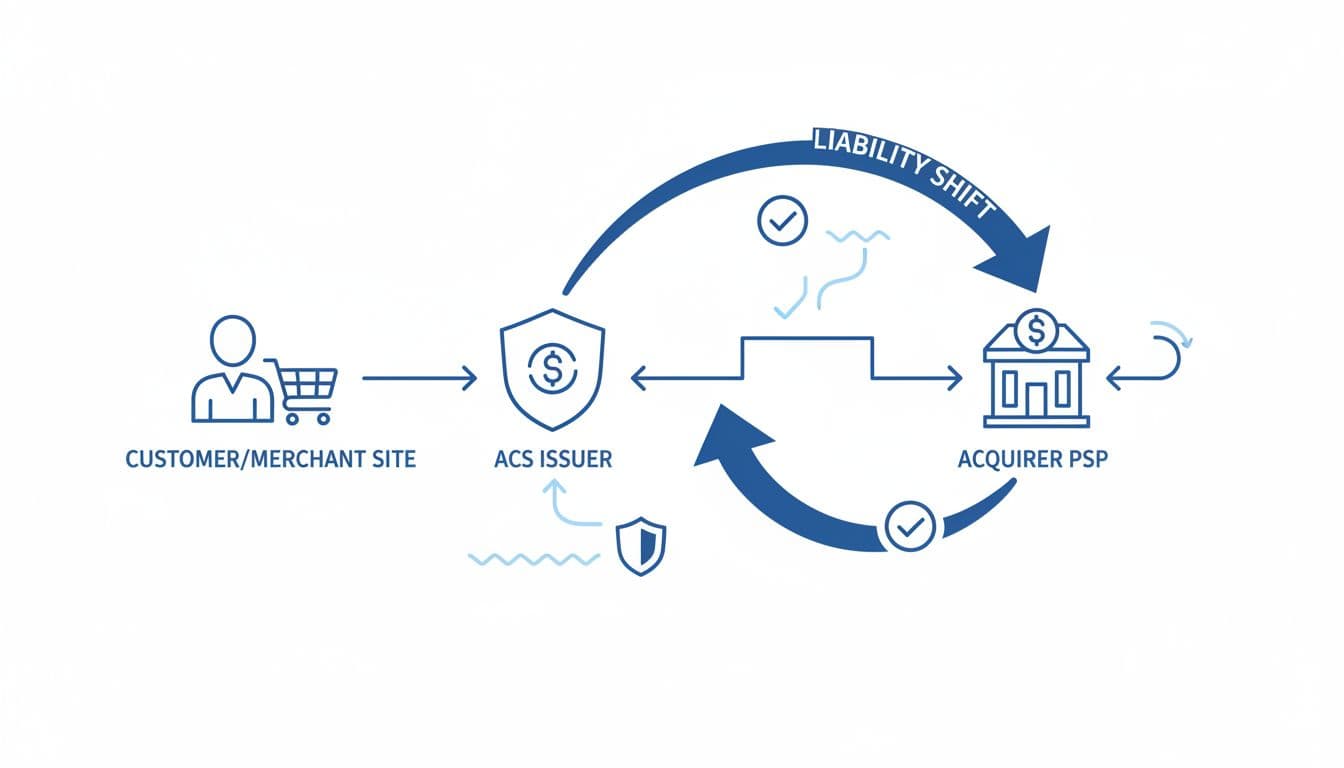

Think of 3D Secure as a bouncer at checkout. If the right customer gets through after bank-backed authentication, the issuer usually takes the fraud risk, not you. As of March 2026, that basic rule still holds across major card brands, including Visa, Mastercard, and Amex.

That said, the shift only applies to fraud-related disputes after a properly authenticated transaction. If a customer says the product never arrived, the service was poor, or a renewal was confusing, the merchant still owns that dispute. If you need a quick refresher on the dispute itself, this guide on chargeback basics for merchants lays out the lifecycle clearly.

For a technical summary, IXOPAY’s explanation of liability shift makes the same point: successful authentication can move fraud chargeback liability, but it does not erase normal merchant responsibilities.

This quick table shows where the line usually sits:

| Scenario | Liability shift? | Who still carries risk? |

|---|---|---|

| Stolen card, successful 3DS auth | Yes, usually | Issuer |

| Product not received | No | Merchant |

| Service quality complaint | No | Merchant |

| Recurring SaaS renewal | Usually no | Merchant |

| 3DS failed or unavailable | No | Merchant |

The takeaway is simple. 3D Secure protects against a narrow but expensive slice of disputes, and that slice is fraud.

How 3DS works at checkout in 2026

In practice, 3DS now feels lighter than the old password pop-ups many teams still remember. Most flows use 3DS2, which supports two common paths: a frictionless flow and a challenge flow. In a frictionless flow, the issuer approves based on shared risk data. In a challenge flow, the buyer may confirm with a code, banking app, or biometric step.

For ecommerce, that usually means less checkout friction than before, while still getting fraud coverage when authentication succeeds. For SaaS, the first payment may qualify, but later recurring charges often do not. That’s the catch many subscription businesses miss.

Your gateway or PSP settings also matter. Some challenge preferences can affect whether a frictionless result carries liability shift. So, don’t assume every “authenticated” message means the same thing. Check the transaction record in your PSP and look for the final liability result.

Payment teams still expect wider 3DS use in 2026, especially as risk tools get better at picking when to challenge. This 2026 3D Secure overview reflects that same trend toward smarter, lower-friction authentication.

Where merchants still carry the risk

This is where many teams get burned. They turn on 3DS, see fewer fraud losses, and think the job is done. It isn’t.

If the dispute reason is non-fraud, liability shift usually does nothing. That includes “item not received,” “not as described,” duplicate billing, unclear cancellation terms, and many subscription renewal complaints. In other words, 3DS won’t rescue a weak billing descriptor or a messy refund policy.

3DS can move fraud liability, but it won’t fix merchant error or customer confusion.

SaaS businesses need extra care here. A user may fully authenticate the first payment, then forget the renewal weeks later. If they dispute that charge, the merchant often still owns it. The same applies when authentication fails, the issuer is unavailable, or the transaction never enters a valid 3DS flow.

So, treat 3DS as one lock on the door, not the whole security system. It cuts one type of loss well. It does not replace good support, clear renewal reminders, or strong fulfillment records.

Why 3DS needs backup from chargeback prevention software

The best payment setups pair 3DS with early dispute prevention. That’s where tools like Chargebase come in.

Chargebase is a chargeback prevention and recovery platform built for ecommerce and SaaS merchants. It helps reduce the number of chargebacks by connecting to payment providers, spotting dispute signals early, and helping teams act before a case turns into a formal chargeback. It also works with networks such as Ethoca, Verifi CDRN, and RDR, so merchants can stop many cases at the pre-dispute stage.

That matters because 3DS covers fraud, while alert networks help with the rest, especially confusion, billing issues, and friendly fraud. Chargebase also focuses on automation. Merchants can set rules, receive real-time alerts, and use a pay-per-alert model instead of paying for broad fixed tooling. If you want to see how alert networks fit into the picture, this page on Ethoca alerts for early chargeback prevention gives a useful overview.

Most teams get the best results from a layered approach:

- 3DS cuts eligible fraud chargebacks at checkout.

- Dispute alerts help stop non-fraud and friendly fraud before escalation.

- Automation rules speed up refunds or responses when every hour counts.

Chargebase’s own docs on using alerts to keep chargeback ratios low make that link clear: fewer formal chargebacks usually means less processor pressure and less back-office drag.

The bottom line for 2026

In 2026, 3D Secure liability shift still gives merchants real protection, but only in the right cases. It can move fraud liability to the issuer after successful authentication, yet it won’t shield you from service issues, delivery claims, or many recurring SaaS disputes. The smart move is to use 3DS for fraud, then add chargeback prevention software like Chargebase to catch the disputes 3DS can’t stop.

You might also want to read

Uncategorized

Jun 07, 2026

Uncategorized

Jun 06, 2026

Manual vs. Automated Processes

Jun 05, 2026

Uncategorized

Jun 04, 2026