Why Chargebacks Happen in Ecommerce and SaaS and How to Prevent Them

Mar 22, 2026

If ecommerce chargebacks feel random, they aren’t. Most start with a small break in trust: a stolen card, a late package, a vague billing name, or a customer who disputes first and asks later.

For ecommerce and SaaS companies, that matters because a chargeback is more than a lost sale. It can bring fees, manual work, and pressure from processors if dispute rates stay high. Recent 2026 estimates suggest global ecommerce chargeback volume could reach 337 million cases, so this is no small back-office issue.

Most chargebacks start with fraud, confusion, or merchant error

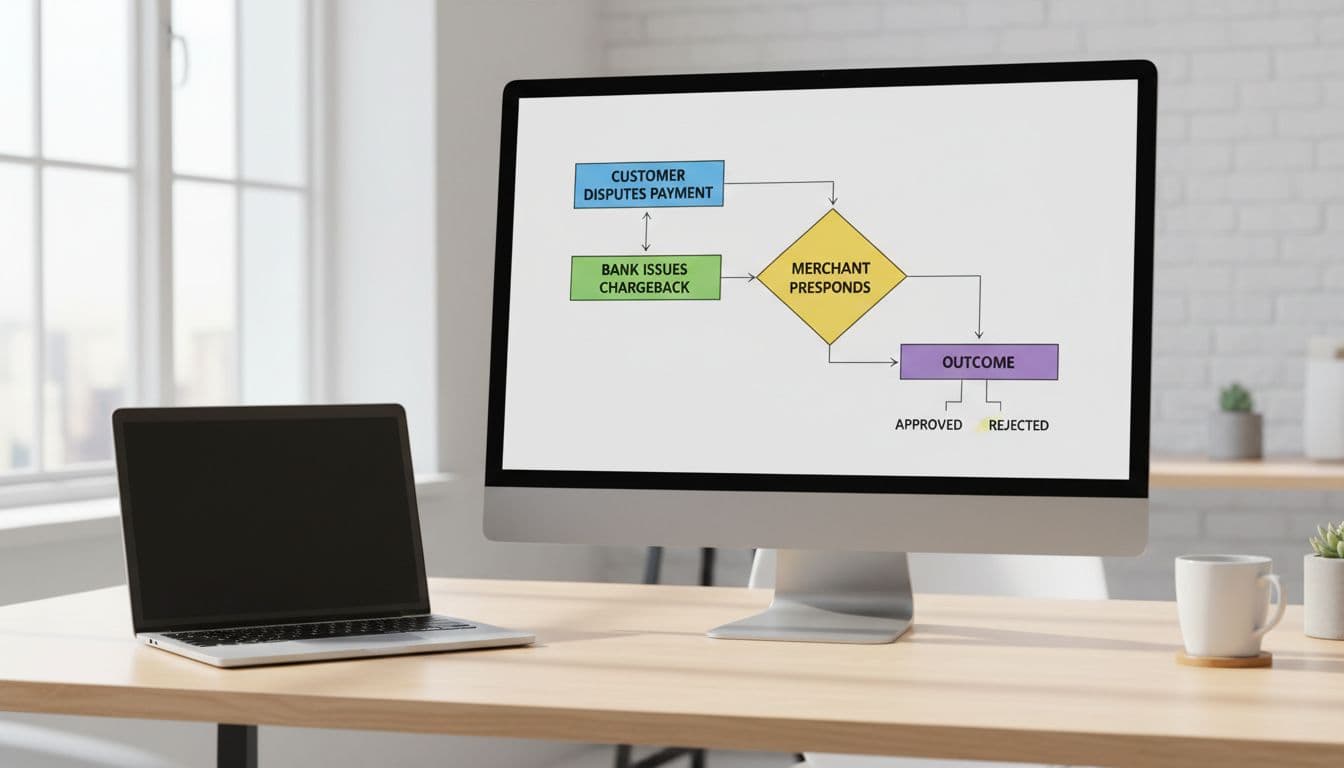

A chargeback is a forced payment reversal started by the customer’s bank. Unlike a refund, it doesn’t begin with your support team. The issuer pulls funds back through the card network, and the merchant often pays a separate fee. If you need a quick primer on the lifecycle, Chargebase has a helpful guide on understanding chargebacks.

The path is usually short and brutal. First comes a complaint or pre-dispute. Then the bank assigns a reason code and pulls the funds. Your team has days, not weeks, to match the order, find proof, and decide whether to fight or refund. Even when the merchant wins, the time cost rarely comes back.

Online sellers get hit harder because card-not-present payments carry more doubt. Nobody sees the card, signs a receipt, or walks out with a bag. In addition, ecommerce adds delivery delays, porch theft claims, and more room for statement confusion. Industry estimates put average online chargeback rates around 0.6% to 1%, which is higher than in-person card use.

Three patterns show up again and again, and they match many published reviews of common chargeback causes:

- Friendly fraud: The customer made the purchase, then disputes it later. Sometimes it’s buyer’s remorse. Sometimes they forgot the order, didn’t recognize the statement descriptor, or a family member used the card.

- True fraud: A stolen card, account takeover, or fake identity leads to a real unauthorized purchase. This stays common in digital goods, high-risk categories, and rushed orders.

- Merchant error: Duplicate billing, late delivery, unclear return rules, poor support, or the wrong item can all push a customer to their bank.

A chargeback is often the final symptom of a broken buying experience, not just a payment event.

That matters because many cardholders never contact the merchant first. Recent research suggests 52% skip support, 72% don’t know the difference between a refund and a chargeback, and 84% see the bank route as easy.

Why SaaS and subscription businesses get hit so often

SaaS has no shipping box to lose, yet disputes happen all the time. The usual trigger is billing confusion. A free trial converts. A customer forgets they signed up. Finance sees a brand name on the statement that doesn’t match the product name and flags it as fraud.

Recurring billing adds another layer. Even satisfied users may dispute a renewal if cancellation felt hard or the price changed. Meanwhile, weak onboarding creates a different problem. If the buyer never reaches value, they may say the service wasn’t as described.

Digital products also make proof harder. You may have login records, IP data, seat activity, and support history, but the cardholder can still claim they didn’t authorize the charge or didn’t get what they expected. That is one reason friendly fraud has become such a large share of disputes. Recent 2026 estimates suggest it may account for 70% to 80% of cases.

Team-based buying adds another trap. One employee starts a trial, another reviews the card statement, and the charge gets disputed because nobody connects the dots. In B2B SaaS, that kind of internal confusion can look exactly like fraud.

For SaaS teams, the weak spots are usually simple: clear billing descriptors, visible renewal reminders, easy cancellation, fast replies, and a clean record of account use. When one of those pieces is missing, a dispute becomes the easiest button to press. If your business sells digital services or subscriptions, many of the same patterns appear in this overview of ecommerce chargeback challenges.

The refund amount is only the start. Most chargebacks also bring a dispute fee, lost product or service time, staff hours, and a mark against your dispute ratio. Some 2026 estimates say merchants lose $3.35 to $4.61 for every $1 tied to fraud once fees and labor are counted. If rates climb too high, processors and card networks may place the merchant in a monitoring program.

That is why early prevention works better than fighting every case after the fact. Chargeback alerts give merchants a short window to act before a dispute becomes formal. In many setups, the best move is simple: refund fast, stop shipment, or cancel the subscription before the bank posts the case. Chargebase explains how Ethoca stops disputes and why that early-warning layer matters.

A good prevention playbook is boring on purpose. Match every alert to an order fast. Check tracking, login history, IP, device, prior refunds, and customer messages. Then pick the lowest-cost safe action.

Chargebase is chargeback prevention software built for merchants that take card payments through gateways and fintech systems. It connects to a payment provider in about two minutes, flags likely disputes early, and helps teams act before they turn into chargebacks. It also supports programs like Ethoca, RDR, and CDRN, with real-time alerts, configurable automation rules, and pay-per-alert pricing. In plain terms, most companies can use it to cut avoidable disputes without adding a pile of manual work.

Still, software works best when the basics are solid. Use clear billing names. Send order, shipping, and renewal notices. Make refunds and cancellations easy to find. Add fraud checks where they fit, and review the biggest dispute reasons each month. Chargebase also shares practical advice on how to lower chargeback rates. If you want a broader look at recurring patterns, this roundup of chargeback risk factors is useful too.

The bottom line

Chargebacks happen when trust breaks, before the sale, during fulfillment, or after billing. Ecommerce businesses deal with fraud and shipping friction, while SaaS teams face renewal confusion and harder-to-prove delivery. The good news is that most disputes leave clues early. Spot those signals, fix the customer experience, and use the right tools, and chargebacks stop feeling random.

You might also want to read

Uncategorized

Jun 07, 2026

Uncategorized

Jun 06, 2026

Manual vs. Automated Processes

Jun 05, 2026

Uncategorized

Jun 04, 2026