Authorization Chargebacks Explained for Ecommerce and SaaS Merchants

Apr 17, 2026

A card payment can be approved in seconds and still come back as a chargeback days later. That gap surprises a lot of merchants, especially when the order looked clean and the customer got the product or service.

For ecommerce and SaaS teams, authorization chargebacks usually point to a payment-process problem, not a product problem. Once you know where authorization broke down, prevention gets much easier.

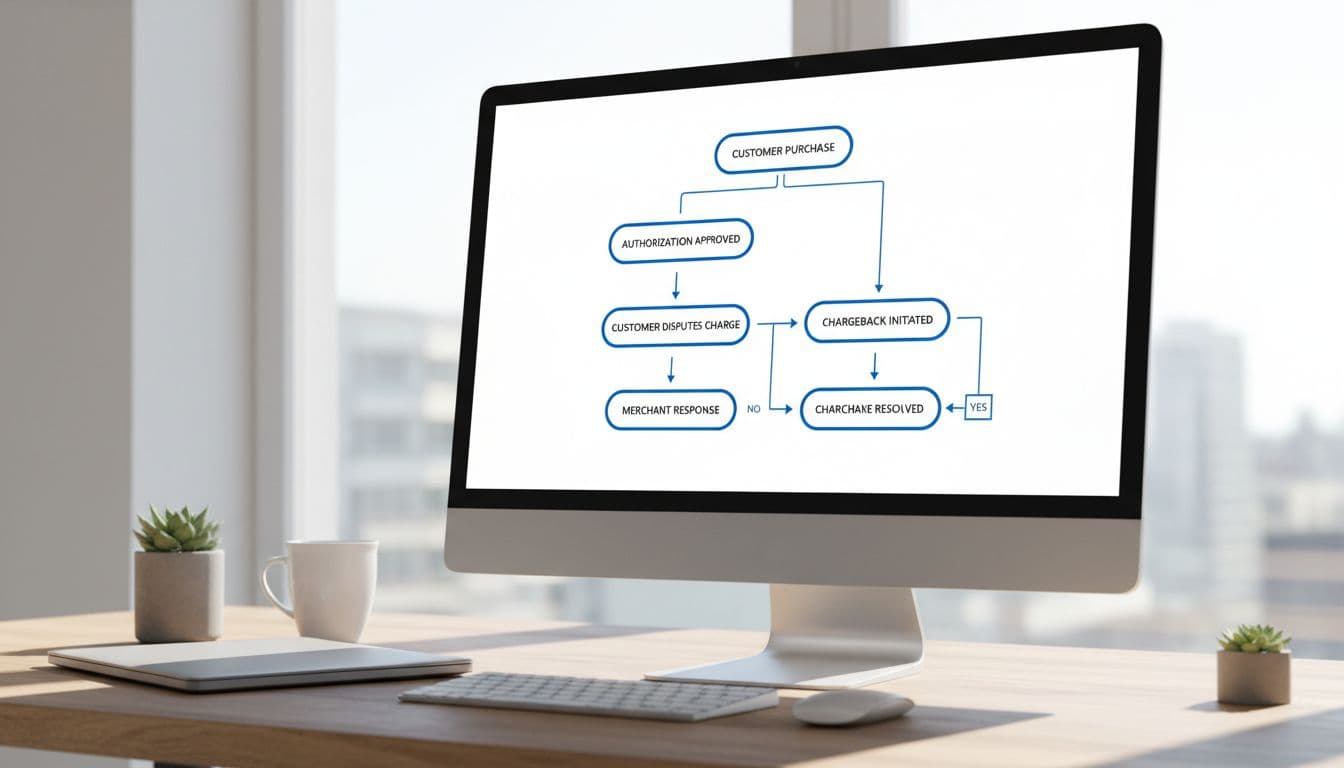

An authorization is the bank’s first approval. It confirms that the card can be used for that amount at that time. It does not mean the merchant can capture funds whenever or however they want.

An authorization chargeback happens when the issuer or card network says the transaction was settled without valid approval under network rules. That can mean no authorization was obtained, the merchant captured after the authorization expired, or the final amount no longer matched what was approved. In SaaS, stored credential and recurring billing rules can also play a role.

This is why an approved order can still turn into a dispute later. The payment looked fine at checkout, but the follow-up steps didn’t match the rules.

If you need a quick refresher on chargeback basics, start there first. It also helps to remember that a bank-led dispute is different from a voluntary refund. The gap between the two shapes how fast you need to act.

A payment approval confirms the issuer accepted the request at that moment. It does not waive the card network’s authorization rules.

Where ecommerce and SaaS merchants get tripped up

Most authorization chargebacks come from timing errors, amount changes, or poor recurring billing setup. Ecommerce merchants often run into trouble when shipment is delayed and the original authorization expires. SaaS teams see similar problems when a rebill happens after card details, consent, or stored credential settings no longer line up.

This quick comparison shows where those issues usually start:

| Trigger | Ecommerce example | SaaS example |

|---|---|---|

| No valid authorization | Order captured after the auth window closed | Rebill submitted without proper stored credential data |

| Amount mismatch | Final capture exceeds approved amount after edits | Upgrade billed for more than the approved amount |

| Late presentment | Backordered item ships too late for the original auth | Invoice captured long after the first approval |

| Consent gap | Customer says merchant charged a saved card incorrectly | Trial converts or renews after weak cancellation records |

The pattern is simple. The farther your final capture moves from the original approval, the more risk you carry.

That matters even more if you use pre-auth flows. This pre-authorization charge guide gives useful background on how holds, capture timing, and settlement affect merchants.

The obvious loss is revenue. The less obvious damage often costs more.

An ecommerce merchant may lose the product, shipping cost, processor fee, and staff time. A SaaS company may lose monthly recurring revenue, spend hours on support, and still pay a dispute fee. If dispute rates rise, processors and card networks may add monitoring, hold funds, or tighten account terms.

Because of that, authorization chargebacks are rarely a one-off annoyance. They can expose weak capture logic, weak billing controls, or weak records around consent and cancellations.

The issue also spreads across teams. Finance sees lost revenue. Support handles complaints. Ops chases evidence. Meanwhile, engineering has to fix the billing flow that caused the problem. Many of the same patterns show up in SaaS chargeback prevention strategies and in post-purchase ecommerce prevention steps, because billing, messaging, and timing often fail together.

Start with the payment rules inside your gateway and billing stack. Re-authorize delayed orders. Capture within the valid authorization window. If the final amount rises, request the right approval first. For subscriptions, store clear proof of consent, keep renewal terms visible, and follow card-on-file rules closely.

Also, review your retry logic. Repeated billing attempts can turn a recoverable payment issue into a dispute. Support and cancellation flows matter too, because a customer who can’t get help may go straight to the bank. If you need a clearer view of the deadlines involved, Chargebase’s guide to chargeback timelines is a useful reference.

Where Chargebase fits

Chargebase is a chargeback prevention software platform built for ecommerce and SaaS merchants. It helps companies reduce disputes by catching issues early, before they become formal chargebacks.

Instead of waiting for the bank to pull funds back, Chargebase connects merchants to early-warning programs such as Ethoca alerts and Verifi-linked tools, including RDR and CDRN. Those programs can surface a dispute in its early stage, so the merchant can refund in time and stop the chargeback from posting.

Chargebase also automates much of the workflow. Merchants can connect a payment provider quickly, set rules for how disputes should be handled, and get real-time alerts only when action can still help. Its pay-per-alert model keeps costs tied to actual use. For most companies that accept card payments, that kind of early automation can lower chargeback volume and cut the manual work around disputes.

A payment approval isn’t the finish line. It’s only the first checkpoint.

When merchants tighten their authorization rules and use early-alert software, authorization chargebacks stop feeling random. They become a measurable process issue, and one you can reduce.

You might also want to read

Uncategorized

Jun 07, 2026

Uncategorized

Jun 06, 2026

Manual vs. Automated Processes

Jun 05, 2026

Uncategorized

Jun 04, 2026