Debit vs Credit Card Chargebacks: What Merchants Need to Know

May 09, 2026

A debit card chargeback doesn’t land the same way as one on a credit card. For the customer, it can tie up their own cash, especially when they dispute a charge for unauthorized transactions. For the merchant, both can mean lost revenue, extra fees, and a higher dispute ratio.

That difference matters if you sell online, run subscriptions, or accept payments through gateways and fintech tools. Once you understand how debit card chargebacks differ from credit card disputes, it’s easier to decide when to refund, when to fight, and where to tighten your process.

Key Takeaways

- Debit card chargebacks pull directly from the customer’s bank account under EFTA/Regulation E, creating more urgency than credit card disputes under FCBA/Regulation Z, which use the issuer’s credit line.

- While credit cards drive higher online chargeback volume (especially friendly fraud and subscriptions), debit disputes often stem from unauthorized transactions or forgotten charges and feel more emotional to the customer.

- Merchants face similar evidence requirements (order proof, delivery, clear descriptors) and costs for both, but keeping chargeback ratios under 1% avoids fees and restrictions.

- Reduce disputes with recognizable billing descriptors, renewal reminders, easy refunds, strong support, and early alert tools like Chargebase to act before cases escalate.

The process looks similar, but the rules behind it don’t

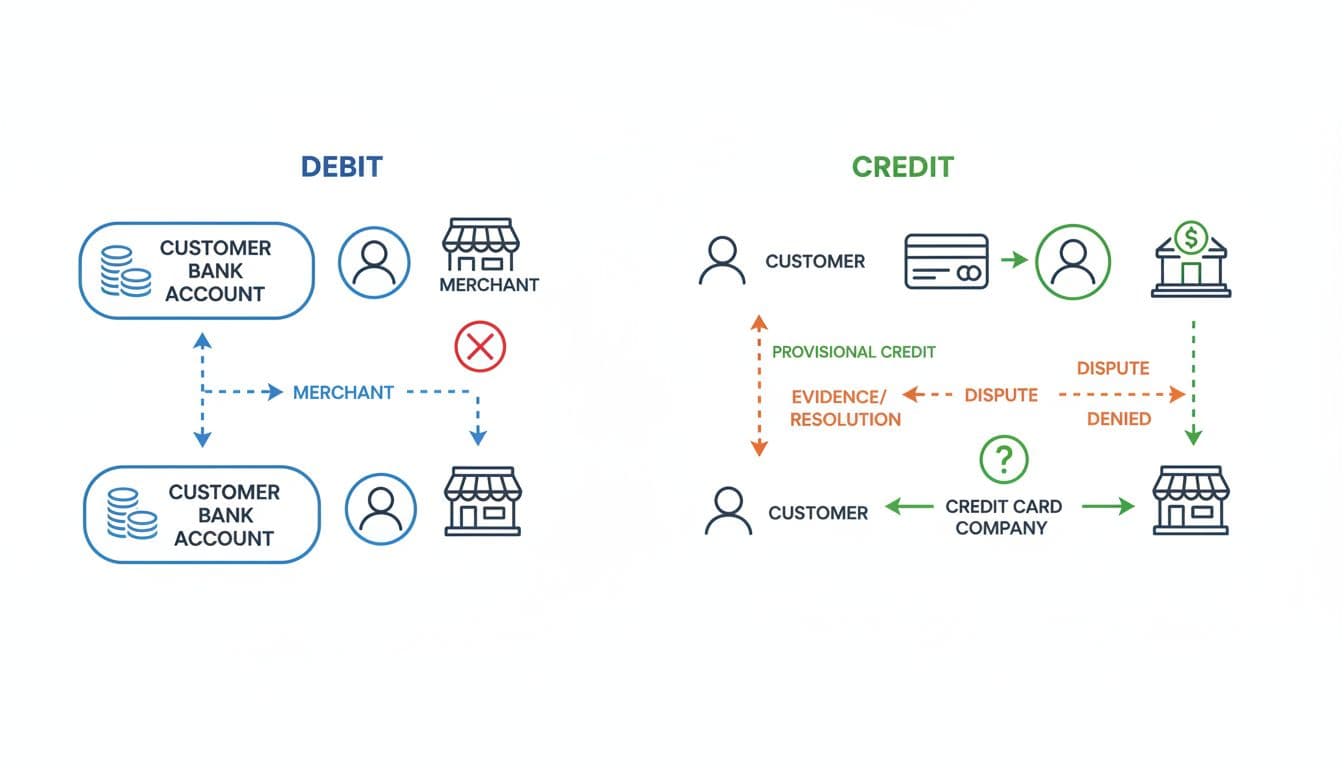

At a high level, both dispute types follow the same chargeback process. A cardholder questions a transaction, the issuing bank opens a case, and the merchant can lose the sale while the bank reviews the evidence. If the case becomes a chargeback, your acquirer usually pulls funds back and may add a chargeback fee.

Under the surface, though, the rules split early. In the U.S., credit card disputes usually fall under the Fair Credit Billing Act framework, while debit card disputes usually follow the Electronic Funds Transfer Act. Investopedia’s overview of chargebacks gives a clear summary of that legal divide.

For merchants, that legal split changes customer behavior more than it changes your paperwork. You still need order records, proof of delivery, billing details, and clean descriptors. Yet the cardholder’s experience is different. With credit, the disputed amount sits on a credit line. With debit, the money often came straight out of the customer’s bank account.

That difference affects volume. Public 2026 data still points to credit cards, especially online, as the larger driver of chargebacks. U.S. merchants are expected to face about 146 million chargebacks this year, worth roughly $15.3 billion. Most of that pressure comes from card-not-present transactions, where friendly fraud contributes to chargeback rates often running higher than in-store rates.

Your chargeback ratio matters no matter which card type caused it. Chargebacks that stack up can trigger fees, reviews, or tougher processing terms. Chargebase’s guide to merchant chargeback rate rules explains why many businesses treat 1% as the line they don’t want to cross when customers dispute a charge.

For most merchants, the biggest split is simple: credit card disputes create more online volume, while debit disputes often feel more urgent to the cardholder because their own cash is already gone.

Key differences between debit and credit card chargebacks

The merchant workflow overlaps, but the customer experience and timing don’t.

This quick comparison shows where the two paths usually separate:

| Factor | Debit card chargeback | Credit card chargeback |

|---|---|---|

| Source of funds | Customer’s bank account | Issuer’s credit line |

| Main U.S. rule set | EFTA / Regulation E | FCBA / Regulation Z |

| Cardholder liability | Stricter timelines under Regulation E | More flexible under Regulation Z |

| Customer relief during review | Often slower or bank-dependent | Provisional credit is more common |

| Common merchant pattern | Lower overall volume, more card-present or stolen-card issues | Higher online volume, more friendly fraud and subscription disputes |

| Customer mindset | Cash is missing now | Customer may feel safer disputing bank-funded credit |

| Merchant evidence needs | Order proof, usage, delivery, descriptor, support records | Mostly the same evidence set |

That table doesn’t mean debit disputes are easier. In some ways, they can be harder to calm down. If a customer sees money missing from a checking account, they may act fast to dispute a charge with the bank before they contact you, particularly for unauthorized transactions. ChargebackHelp’s comparison of debit and credit chargebacks notes that debit cardholder liability and timing rules can be stricter, including the zero liability policy with tight reporting deadlines. Meanwhile, Experian’s chargeback explainer points out that cardholders often receive temporary credit faster on credit card disputes than on debit card disputes.

From the merchant side, the burden of proof feels familiar in both cases. You still need to show that the cardholder authorized the purchase, there was no billing error, they received the goods, or used the service. That’s why operational basics matter so much: clean receipts, easy-to-read billing descriptors, proof of delivery, clear renewal notices, responsive customer service, and fast support.

In short, a debit dispute and a credit dispute may look alike in your dashboard. They don’t feel alike to the person who filed them, and that shapes how often disputes happen and how quickly they escalate.

Why debit card chargebacks can hit differently

A debit card chargeback often starts with raw urgency. The customer isn’t looking at borrowed money. They’re looking at money that may have paid rent, payroll, or groceries. That makes patience harder, especially when they suspect fraudulent charges or unauthorized transactions, the descriptor is vague, or the purchase came from a subscription they forgot about.

For merchants, lower debit dispute volume can create false comfort. Credit cards still produce more chargebacks overall, especially in ecommerce. Yet a debit dispute can still cost you the product, the revenue, the shipping, and the labor needed to respond. In 2026, merchants still lose several dollars in total cost for every $1 lost to fraud or chargebacks once fees and operational work are added.

Friendly fraud makes both card types harder to manage. Current industry data suggests a large share of disputes come from friendly fraud, customers challenging valid transactions like recurring payments, merchant error, and many cardholders still don’t understand the difference between a refund and a chargeback. Chargebase’s explanation of refunds versus forced chargebacks is useful here, because the two paths lead to very different costs for the merchant.

This is why “debit vs credit” isn’t only a banking topic. It’s a support and billing topic too. If a customer can’t recognize the charge, can’t reach your customer service, or can’t cancel quickly, the bank becomes the next stop to dispute a charge. That is true for physical goods, but it’s even more common with SaaS, digital access, renewals, and subscription services.

So while debit card chargebacks may be fewer, they still deserve their own playbook. The trigger is often more emotional, the customer feels the loss sooner, and the window to defuse the problem may be short.

How merchants can reduce both debit and credit card chargebacks

Most businesses don’t need separate teams for debit and credit disputes. They need one clear system that catches issues early and responds fast.

Start with the basics that reduce disputes before they start:

- Use billing descriptors customers can recognize on a bank statement to aid fraud prevention and cut debit card chargebacks.

- Send renewal reminders and receipts with plain language.

- Make refunds easy to request and easy to understand, aligned with your refund policy.

- Keep delivery, login, usage, support records, address verification service results, authorization codes, and compelling evidence organized.

- Review disputes by source, product, country, and payment method, so patterns show up early.

After that, speed matters. If a customer goes to the bank first, your best chance may be an early alert before the case becomes a formal chargeback. That’s where chargeback prevention software helps.

Chargebase is a chargeback prevention platform built for merchants that accept card payments through gateways, digital wallets, and other fintech systems. It is an official Ethoca and Verifi partner, and it helps companies cut disputes before they become full chargebacks. The setup is designed to be quick, often with a no-code connection to the merchant account via the payment provider, and the workflow is simple: connect, detect risk, and act before the dispute turns into a network case.

The platform automates much of the chargeback cycle, sends real-time alerts when there’s still time to stop a dispute, and supports rule-based handling through network programs such as Ethoca, CDRN, and RDR. If your team wants a better sense of those programs, Chargebase explains how Ethoca provides early chargeback alerts and also breaks down Verifi RDR explained.

That matters because many disputes are preventable if you refund quickly enough. Chargebase also uses performance-based pricing, so merchants pay per alert instead of carrying a large fixed cost. For ecommerce and SaaS brands looking to improve customer service and prevent customers from trying to dispute a charge, that can be a practical way to reduce debit card chargebacks, credit card disputes, and the operational drag that comes with both.

Frequently Asked Questions

What’s the key legal difference between debit and credit card chargebacks?

Debit chargebacks fall under the Electronic Funds Transfer Act (EFTA/Regulation E) with stricter timelines and customer liability rules. Credit chargebacks follow the Fair Credit Billing Act (FCBA/Regulation Z), often providing faster provisional credits. For merchants, this mainly affects customer behavior more than the dispute process itself.

Why do debit card chargebacks feel more urgent to customers?

With debit, the disputed amount comes straight from the customer’s bank account, tying up their own cash for essentials like rent or groceries. Credit disputes use borrowed funds, so customers may feel less immediate pressure. This urgency can lead to faster disputes before contacting the merchant.

Do merchants need different evidence for debit vs. credit chargebacks?

No, the evidence set is largely the same: order records, proof of delivery or usage, billing descriptors, authorization details, and support logs. Clear documentation helps win representment regardless of card type. Focus on basics like AVS results and customer communications to strengthen cases.

How can merchants cut chargeback risk for both card types?

Use clear, recognizable billing descriptors, send renewal reminders, make refunds straightforward, and maintain organized records. Tools like Chargebase provide early alerts via Ethoca and Verifi to refund proactively before formal chargebacks. Monitor ratios by payment method to spot patterns early.

Are debit card chargebacks less common than credit ones?

Yes, credit cards produce more overall volume, especially in ecommerce and card-not-present transactions. Debit disputes are lower but can be harder due to customer cash impact and stolen-card issues. Both threaten revenue, fees, and processing terms if ratios climb.

Final thoughts

Debit and credit chargebacks share the same headache, but they don’t start from the same place. Debit disputes involve a customer’s own cash, while credit disputes often come with faster temporary relief and more online volume.

If your team treats every dispute the same, you’ll miss what drives them, such as fraudulent charges or merchant error. The best defense is still simple: prioritize fraud prevention to safeguard your bottom line, make charges easy to recognize, fix support gaps fast, and use early alerts before a dispute tied to a specific reason code escalates through payment card networks to representment or arbitration, becoming a fee, a lost sale, and a ratio problem.

You might also want to read

Uncategorized

Jun 07, 2026

Uncategorized

Jun 06, 2026

Manual vs. Automated Processes

Jun 05, 2026

Uncategorized

Jun 04, 2026