Chargeback vs Refund vs Reversal vs Void, what each one means in Stripe, Shopify, and most gateways

Feb 10, 2026

Ever look at a transaction and think, “We gave the money back, so why does it still look bad?” That confusion usually comes from mixing up chargeback vs refund (and the other two “undo” options: reversal and void).

They all move money in the opposite direction, but they don’t mean the same thing to card networks, banks, Stripe, Shopify, or your finance team. Timing, who starts the action, and whether it becomes a dispute record are the real differences.

If you manage a merchant account with your payment processor, getting these terms right helps you choose the cheapest, safest outcome before a simple support issue turns into a chargeback.

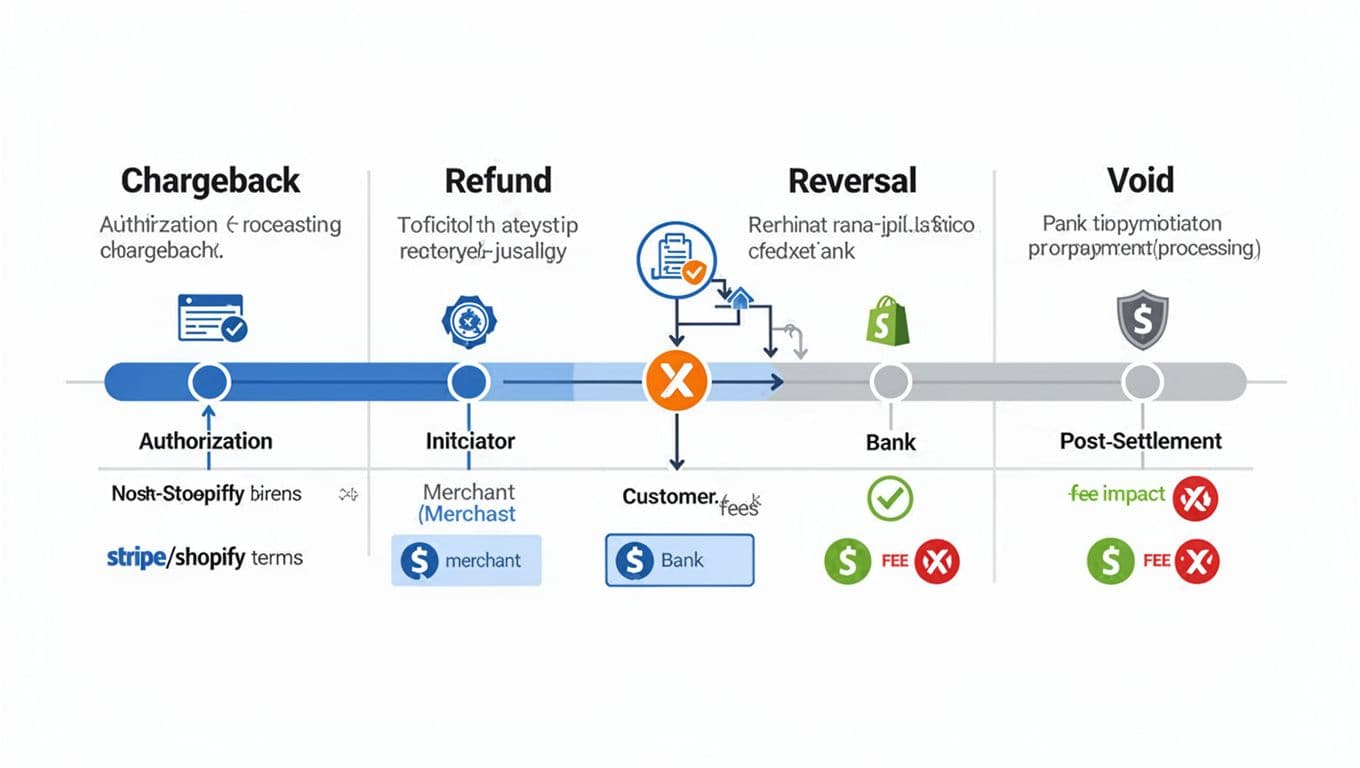

The simplest way to tell them apart is timing (and who’s in control)

A card payment has phases: authorization (the “hold” for a pending transaction), capture (you take the funds), then settlement (money moves through the network). An authorization reversal releases the hold before it completes. Each “undo” option sits in a different spot on that timeline.

Here’s the practical meaning most teams need:

| Outcome | What it means in plain English | Typical timing | Who starts it | Why it matters |

|---|---|---|---|---|

| Void | Cancel an uncaptured charge (void transaction) so it never settles | Same day, before settlement | Merchant | Usually the cleanest undo, often avoids extra risk signals |

| Reversal | A broader “stop it before it completes” action (often a payment reversal or authorization reversal) | Before settlement, sometimes right after auth | Processor, bank, or merchant (depends on gateway) | Often looks like the payment “disappears” instead of being refunded |

| Refund | Return money after the charge has been captured | After capture or settlement | Merchant | Customer gets money back, but it’s still a completed sale that got reversed |

| Chargeback | The cardholder asks their issuing bank to pull money back | After settlement (days to weeks later) | Cardholder via issuing bank | Highest operational cost, can include fees, and counts toward dispute rates |

A good mental model: void/reversal is like canceling a restaurant order before it hits the kitchen, refund is sending the dish back after it’s served, and a chargeback is calling your credit card company after you leave and forcing the restaurant to fight it out.

Card networks and card issuers have treated these outcomes the same way for years, and as of 2026 the core differences still come down to timing, initiator, and dispute impact. Stripe has a solid primer on what happens during disputes in its guide to chargeback basics for businesses.

What these actions look like in Stripe, Shopify, and most payment gateways

Even though the core rules are shared across card networks, the labels you see change a bit by platform in Stripe, Shopify, and most payment gateways.

In Stripe: “refund” and “dispute” are clear, “void” is usually a cancel-before-capture

In Stripe, the clean split is this:

- If you haven’t captured the funds yet (common with separate auth and capture), you can usually cancel the payment. In day-to-day ops, many teams call that a “void”, because the goal is the same (prevent settlement).

- If you have completed the capture transaction, you issue a refund. The charge stays in your transaction history as a successful payment that was later refunded.

- If the customer goes to their bank, Stripe shows it as a dispute (the Stripe term for chargebacks and dispute stages). At that point, you’re in a dispute process, not a simple customer service flow.

In Shopify: the admin often shows “refund” for post-capture, and “void” only in narrow cases

Shopify and Stripe rank among the most common platforms, but Shopify sits on top of a gateway (Shopify Payments, PayPal, Authorize.net, and others). That’s why the same action can look different depending on the gateway settings and where the payment is in the lifecycle.

In most Shopify setups:

- If the transaction is still pending and hasn’t settled, you may be able to void it (or Shopify may show it as canceled).

- If it’s already processed, you’ll do a refund tied to the order.

- If the bank gets involved, Shopify surfaces it as a chargeback in the admin, and you respond with order details, delivery proof, logs, or policies.

In “most gateways”: reversals are often automatic, and voids are time-sensitive

Many processors use “payment reversal” to describe what happens when:

- an authorization expires,

- a duplicate auth is corrected,

- the processor or issuer drops the hold,

- you cancel before capture.

In these scenarios, the cardholder receives their funds back to the original payment method, which is why payment reversals can feel mysterious. They may not be a button you clicked, but they still affect reconciliation.

If you want a clear, gateway-agnostic breakdown of the wording gap, this explanation of payment reversal vs refund differences is useful, especially for finance and support teams trying to line up terminology.

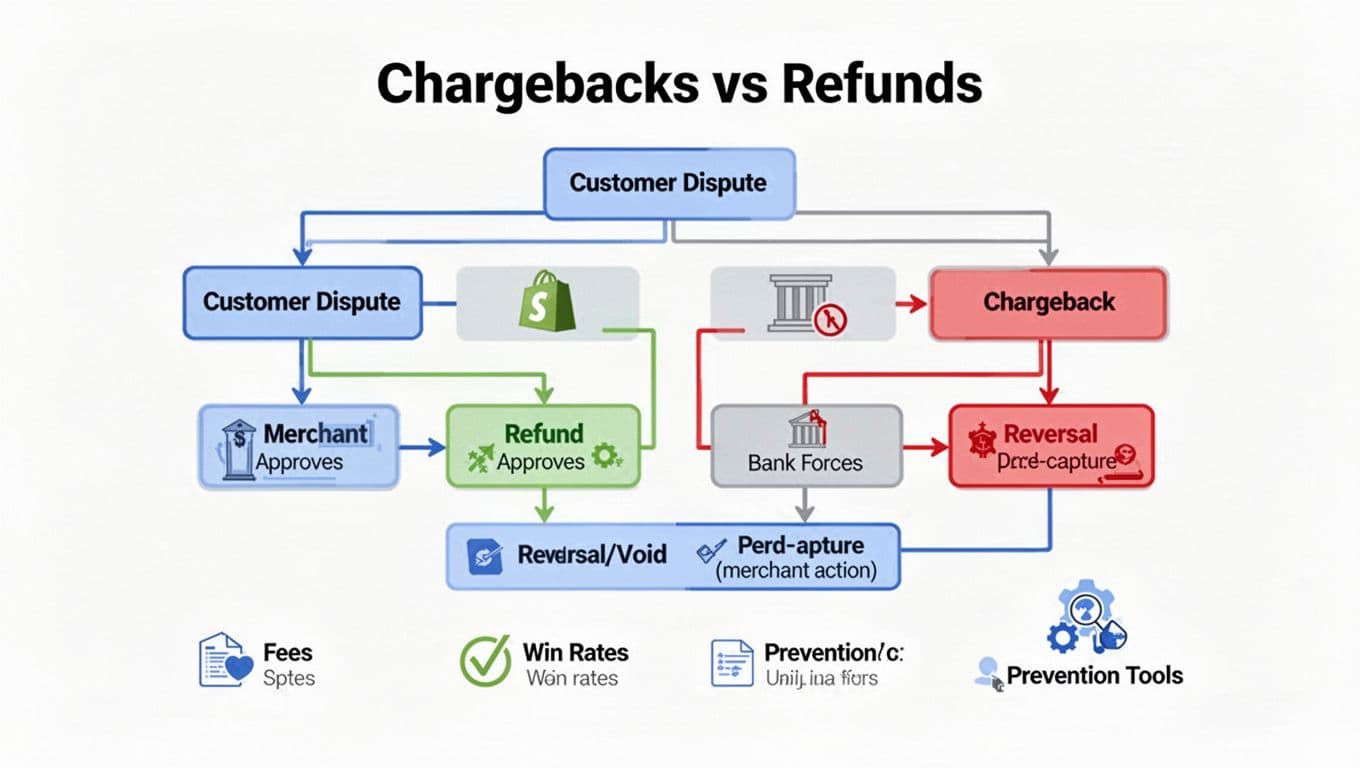

The money part: fees, risk, and how to avoid chargebacks before they start

Chargebacks cost more than the transaction amount due to chargeback fees and revenue loss. You often lose the sale, pay dispute fees, and spend time gathering evidence. Too many can also raise your risk profile with processors and card networks, which can lead to monitoring programs, stricter terms, or account limits.

Refunds usually hurt less because you control them. They’re also fast social proof to the customer that you listened. A clear return policy and good customer support can prevent a refund from becoming a dispute. A refund won’t automatically “fix” a bad experience, but it often prevents the customer from escalating to their bank.

Voids and reversals are usually the least painful because they stop settlement or unwind the payment before it becomes a completed sale. When you can use them, they often reduce downstream noise in disputes reporting.

A practical rule for choosing the right outcome

If you can still cancel before capture, void/reverse. If the payment is already captured and the customer is unhappy, refund quickly. If the customer has already disputed, often due to friendly fraud, you’re in chargeback territory, and prevention is no longer the main play.

Where Chargebase fits for teams trying to reduce disputes

The hard part is speed. Most businesses don’t lose disputes because they had no evidence, they lose because the issue reached the bank before the business acted. Even when fighting the dispute process, merchants need compelling evidence for representment, or failing to resolve it could lead to arbitration.

Chargebase is built for that gap. It connects to your payment provider with a no-code setup, then helps merchants prevent chargebacks through networks and programs like Ethoca alerts, Verifi CDRN, and Visa Rapid Dispute Resolution. The idea is simple: get a real-time warning early enough that you can choose a refund (or automated resolution rules) before it becomes a network chargeback.

Chargebase also uses a pay-per-alert model, so costs track usage, not long contracts, and it supports automation rules so your team can standardize what happens for common dispute triggers. If you want a deeper look at issuer alert networks, see Chargebase’s guide on Ethoca chargeback prevention. For ongoing operations, this doc on how to reduce your chargeback ratio maps well to how payment teams actually work.

One more reality check: dispute prevention is not only tooling. Clear billing descriptors, easy cancellation, fast shipping updates, and responsive support cut disputes before they reach the card issuer and alerts even fire.

Conclusion

If you remember one thing, make it this:

- Void transaction and payment reversal happen before settlement,

- Refund happens after capture,

- A chargeback is a bank-led dispute that you don’t control.

The earlier you act, the cheaper the outcome, the cleaner your risk profile looks, and the better the cardholder experience becomes.

Treat refunds as a customer service tool, and treat chargebacks as a process problem to prevent, not just fight. If chargebacks are eating time and margin, chargeback prevention systems like Chargebase can give you earlier signals and automated paths to stop disputes before they become chargebacks, helping prevent revenue loss.

You might also want to read

Uncategorized

Apr 10, 2026

Uncategorized

Apr 09, 2026

Uncategorized

Apr 08, 2026

Uncategorized

Apr 07, 2026