Billing Descriptor Fixes That Cut “Unrecognized Charge” Disputes (Real Examples)

Jan 28, 2026

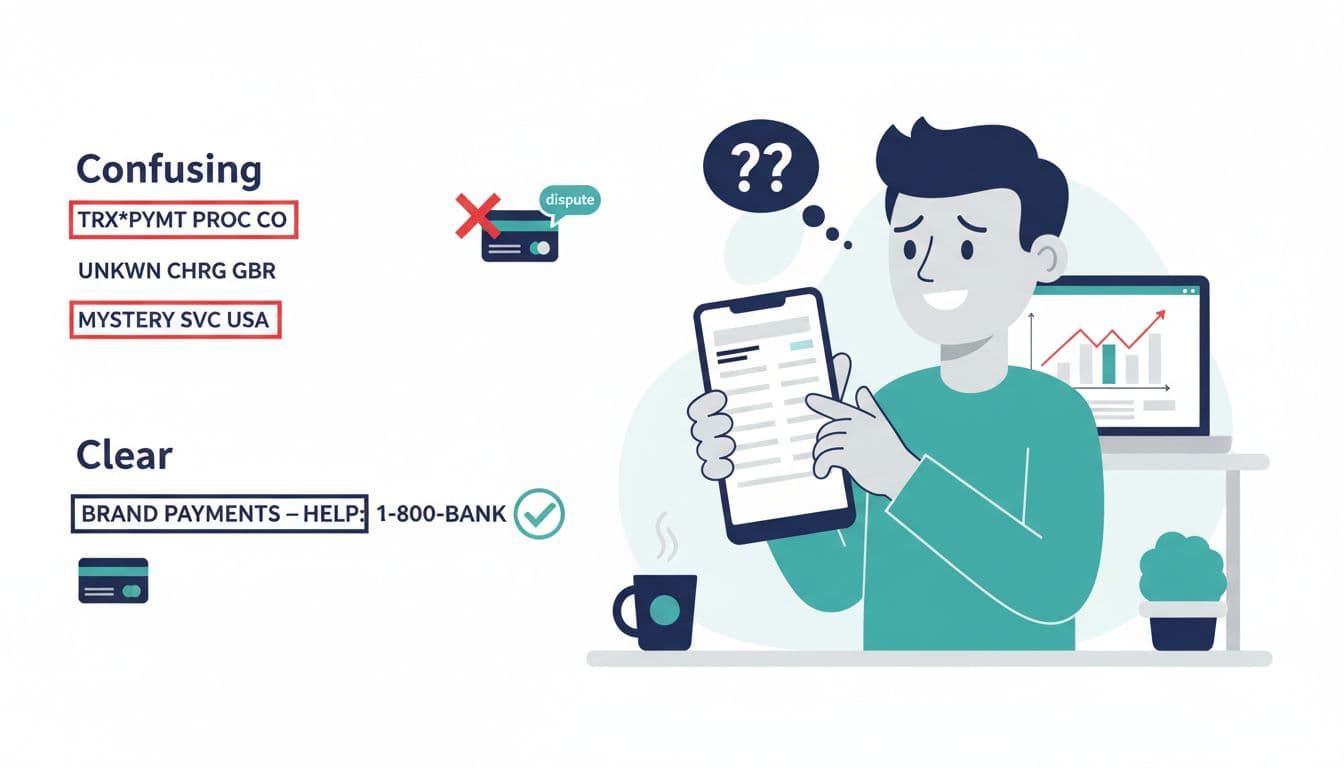

A customer sees an unrecognized charge on their statement that doesn’t ring a bell. They’re busy, they don’t hunt through old emails, and they definitely don’t remember the “legal entity” name behind your brand.

So they do the one thing that feels safest: they contact their issuing bank about the unrecognized charge.

In many cases, this isn’t malicious fraud. It’s friendly fraud from billing descriptor confusion. The good news is you can fix a big chunk of these disputes with a few practical changes, plus a backstop that catches issues before they turn into chargebacks.

Why a billing descriptor causes “unrecognized charge” disputes

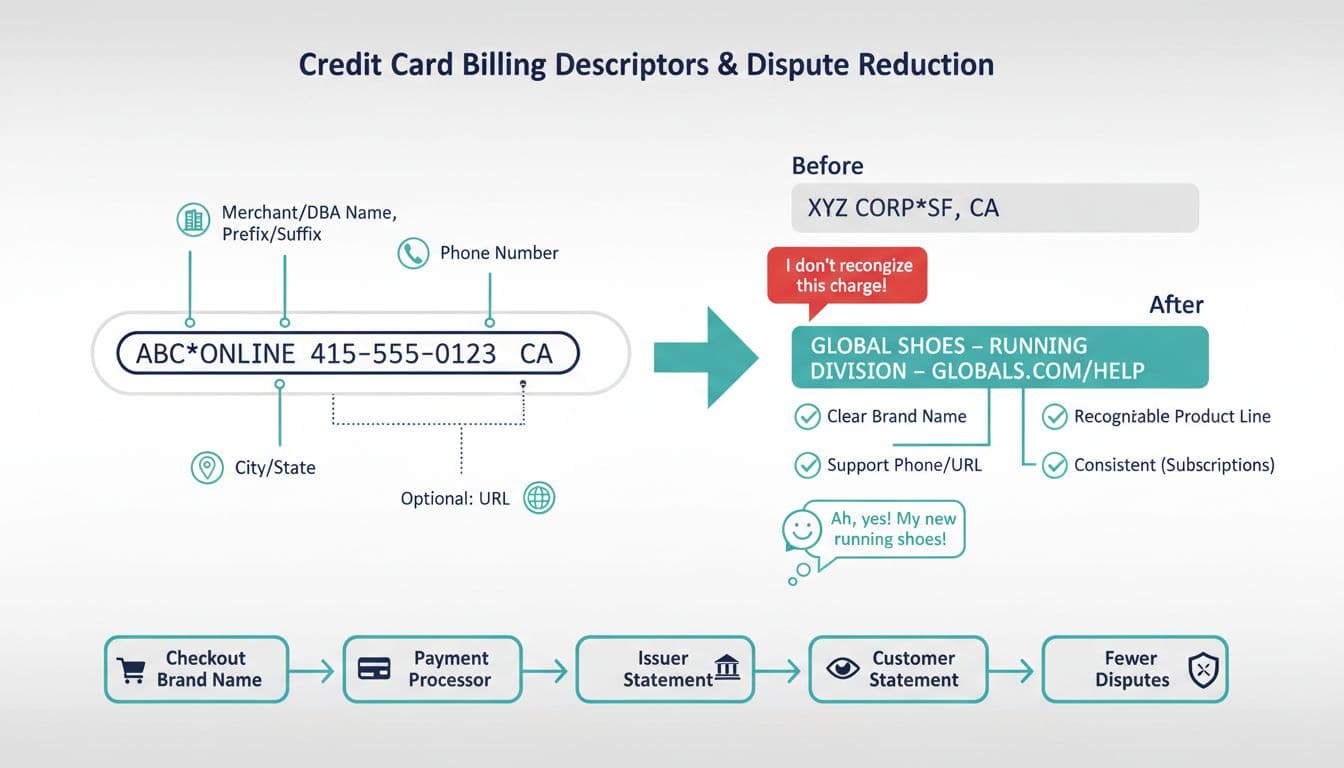

A billing descriptor is the short line a cardholder sees on their billing statement. It’s often the only clue they get when deciding whether a purchase is legit, and unclear ones contribute to first-party misuse.

Here’s why this billing descriptor causes so many disputes:

- Your statement name doesn’t match your brand. The customer remembers “Sunny Skincare,” but the statement says “SSK INC CA.”

- You sell multiple products, but the descriptor is generic. If everything shows up as “ABC*ONLINE,” people won’t connect it to a specific purchase.

- Your customer made a card-not-present purchase through a different flow. They clicked an influencer link, paid through a hosted checkout, or used a saved card. The memory trail is weak.

- Your support info isn’t easy to find. If there’s no helpful phone or URL on the statement line, the bank dispute button becomes the support desk.

Most processors let you set a statement descriptor (and sometimes a dynamic one per product or location). The details vary by provider and network, but the goal is always the same: make the customer instantly think, “Oh right, that’s them.” For a practical breakdown of what descriptors can include and why they matter, see Stripe’s guide to billing descriptors.

Billing descriptor fixes that actually reduce disputes (with before and after examples)

Think of your descriptor like a label on a pantry jar. If it says “SPICE 04,” someone’s going to toss it. If it says “CINNAMON,” it gets used.

Below are real-world style examples you can adapt today to reduce disputes like friendly fraud (the “after” versions aren’t longer, they’re just clearer):

| Scenario | Before (confusing) | After (recognizable) |

|---|---|---|

| E-commerce brand | BRIGHT*SHOP 029394 | BRIGHTHOME DECOR brighthome.com |

| Subscription SaaS | NIMBUS*BILLING | NIMBUS CRM SUBS nimbuscrm.com |

| Fitness membership | GLBL*SVCS 877593 | GREENLEAF GYM 877-555-0199 |

| Digital course | VID*LEARN 1122 | VIDLEARN COURSE support.vidlearn.com |

What changed in the “after” versions?

The brand name is obvious: Use the name customers see at checkout, in emails, and on your site header. Avoid internal abbreviations.

There’s a memory hook: Add a product line, plan, or category when possible (for example, “CRM SUBS” for a subscription business, “MEAL KIT,” “PRO PLAN”). This helps when a customer buys from you more than once.

Support is one step away: A short URL or phone number that reaches a real help path, such as your cancellation policy or refund policy, can prevent panic disputes. If you add a phone number, make sure it’s staffed and your IVR mentions refunds and cancellations early.

Consistency matters more than cleverness: If your checkout says “BrightHome,” your confirmation email says “BrightHome,” but the bank statement says “BHD Holdings,” your customer will assume fraud. Align the words across every touchpoint.

Checkout.com has a solid explanation of how descriptor choices connect to dispute rates in its guide on using billing descriptors to reduce chargebacks. Tools like Visa Order Insight complement this by providing additional data to the customer via the bank.

One quick caveat: if you sell through some app store flows, the statement line may show the platform (not your business). In that case, your best “descriptor fix” is clear receipts, renewal reminders, and fast support.

A simple audit process to clean up descriptor confusion across products

Most descriptor problems persist because teams don’t see the “issuer view.” Marketing sees the brand. Finance sees settlement reports. Support sees tickets. The customer sees one short line. This disconnect harms merchant account health and can trigger fraud detection flags.

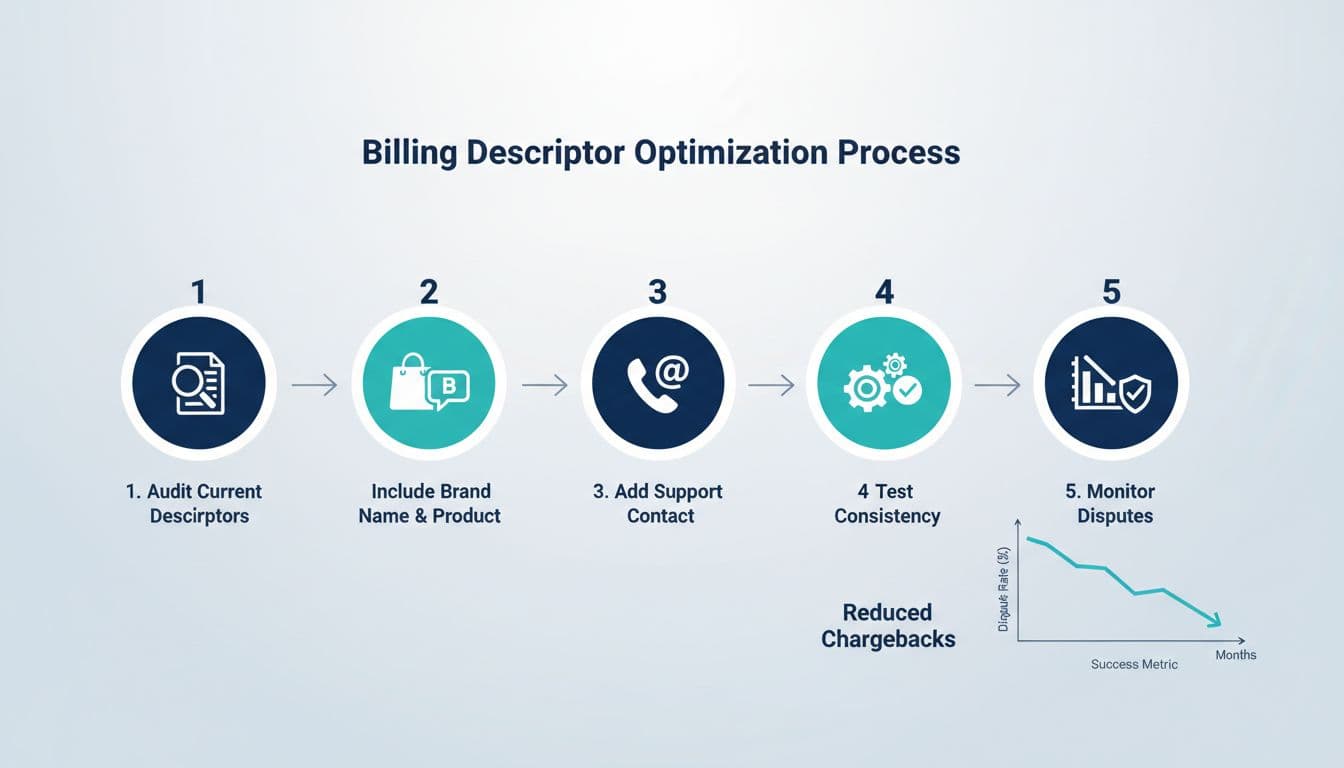

Run this audit like a cleanup sprint:

1) Inventory every descriptor in use

Many businesses have more than one: per payment provider, per region, per MID, per product, per checkout, or per subscription renewal. Make a simple list and note where each one appears.

2) Compare it to what customers remember

Open your last 50 receipts and renewal emails. What brand name is front and center? That’s what should lead the descriptor, not your legal entity. Cross-check with address verification service data to align internal records.

3) Add a “contact path” that actually resolves issues

Pick one: a support phone number that routes to billing, or a short URL that lands on “What is this charge?” plus refund and cancellation steps. The goal is to stop the customer from calling the bank first.

4) Test with small real transactions

Have teammates with different banks run small purchases and screenshot the statement line. Don’t assume it matches what your processor dashboard shows.

5) Track the right dispute bucket

Descriptor work should reduce “no knowledge” or “fraud: cardholder doesn’t recognize” disputes first, helping lower your dispute ratio. If you’re also watching thresholds and monitoring programs like the Visa Acquirer Monitoring Program and its VAMP ratio, a subscription-focused view like Solidgate’s VAMP remediation guide can help you think about dispute rate pressure in a structured way.

When descriptor fixes aren’t enough: stop disputes before they become chargebacks

Even with a perfect billing descriptor and 3D Secure authentication, some customers still dispute. Sometimes they forgot a free trial ended. Sometimes a family member used the card. Sometimes they’re trying their luck.

This is where pre-dispute alerts and auto-refund workflows can save time and reduce chargebacks.

Chargebase is a chargeback management and recovery platform for e-commerce and SaaS teams. It connects to your payment provider quickly (often in minutes, with no code) and uses global merchant data plus network programs like CDRN and RDR to spot disputes early and help stop them before they become chargebacks. These programs operate under rules set by each card network.

Key ways Chargebase helps in practice:

- Real-time alerts when they can prevent a chargeback, so you can respond fast (often by issuing a refund before the dispute escalates).

- Automation rules (10 or more options, depending on the network flow) so refunds and responses follow your playbook, not someone’s inbox.

- Performance-based, pay-per-alert pricing, which keeps costs predictable. For example, pricing can be structured per alert (such as $15 for CDRN alerts, $25 for Ethoca alerts, and $15 for Rapid Dispute Resolution alerts), with enrollment times that vary by network (often hours for some programs, days for others).

If a dispute does escalate, the process can get expensive and slow, with dispute fees piling up as you fight back using compelling evidence for representment and a detailed rebuttal letter. It helps to understand what happens next, including chargeback arbitration, as explained in Stripe’s overview of chargeback arbitration across card networks. Prevention is usually the cheaper path.

Conclusion

“I don’t recognize this charge” disputes often start with a simple mismatch between what customers remember and what their statement shows. Tightening your billing descriptor (brand name, product hint, and a real support path) is one of the fastest ways to cut that noise and bolster consumer protection.

For subscription businesses managing their merchant account, pair those fixes with early-warning alerts, smart automation, fraud detection, and compelling evidence against friendly fraud. You can reduce chargebacks without burying your team in manual work. The statement line is small, but it carries a lot of weight.

You might also want to read

Uncategorized

Apr 10, 2026

Uncategorized

Apr 09, 2026

Uncategorized

Apr 08, 2026

Uncategorized

Apr 07, 2026