How to Build a 30-Day Chargeback Recovery Plan

Apr 04, 2026

Chargebacks can drain margin faster than a weak sales month. You lose revenue to your payment processor, pay fees, and spend team time on cleanup at the same time.

A strong chargeback recovery plan gives you a 30-day reset. Instead of treating every dispute like a surprise, you build a clear system for finding losses, recovering what you can, and developing a chargeback reduction plan to cut future cases before they hit your ratio and damage merchant health.

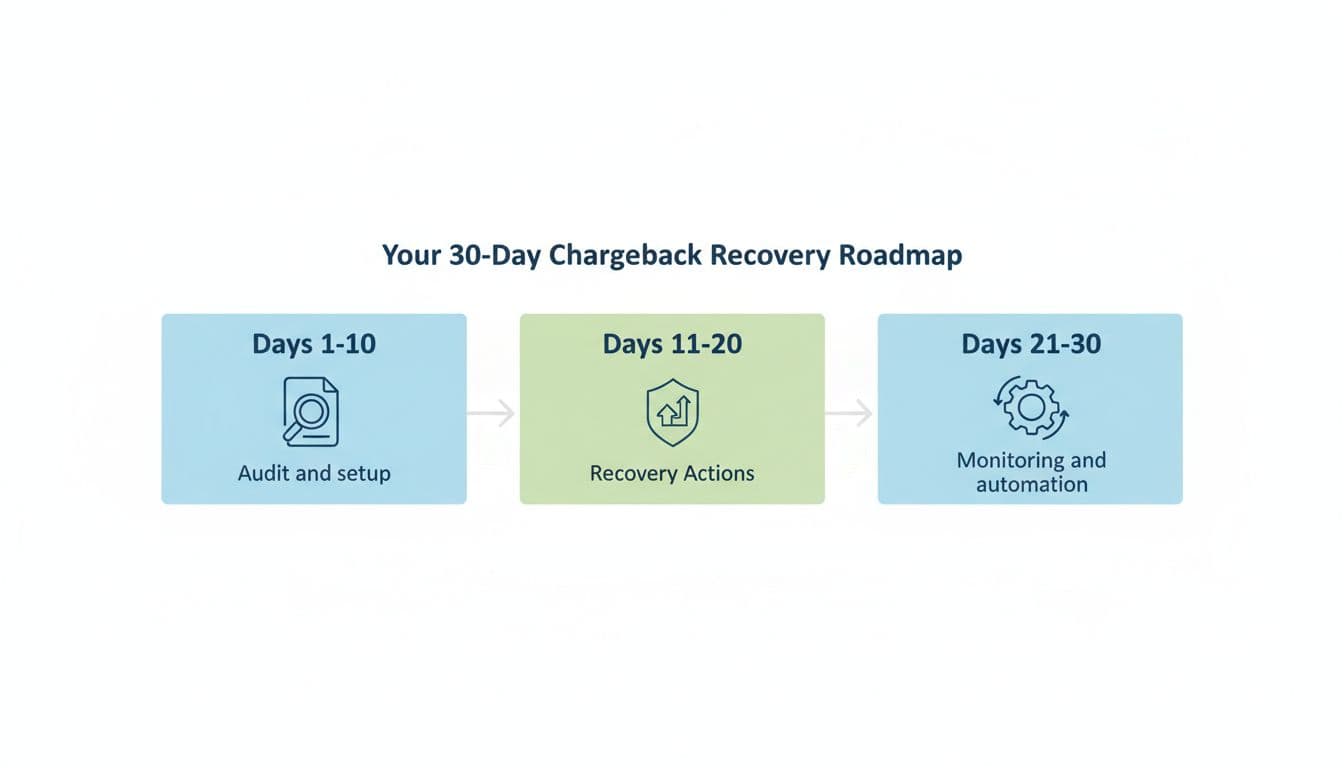

Days 1 to 10, audit the damage and assign owners

When chargebacks rise, many teams rush to fight cases right away. That feels productive, but it usually creates more noise. First, get a clear picture of the problem.

Start with the basics. If newer team members need a refresher, this guide on understanding chargebacks explains how the issuing bank starts disputes, why they hurt revenue, and how short response windows can be. Then pull at least 90 days of transaction data. If your volume is lower, go back six months.

Group disputes by reason codes, product, gateway, card brand, country, subscription plan, and fulfillment status. Use root cause analysis to separate three buckets: true fraud (such as card-not-present fraud), merchant error, and first-party fraud, also known as friendly fraud. That split tells you where to act first. For example, “product not received” points to shipping or support. “Fraud” may point to weak screening. “I didn’t recognize this charge” often points to a confusing billing descriptor.

Recent 2026 chargeback statistics show the damage goes well past the sale amount. The chargeback fee, labor, lost goods, and processor pressure all pile on.

Next, build a small working group. Finance should own reporting. Support should own customer context. Ops or fulfillment should own delivery facts. If you run subscriptions, add billing. Give the group one queue, one daily review time, and one owner for final decisions.

By day 10, you should have a ranked list of dispute causes, a clear owner map, refund rules for common cases, and a shared evidence folder. That foundation matters because weak recovery usually starts with messy intake, not bad intent.

Days 11 to 20, recover revenue and stop the easy losses

Now move from diagnosis to action. Think of this phase like an emergency room triage desk for dispute resolution. Every case does not deserve the same treatment, and speed often beats perfection.

Use a simple decision model for the next 10 days:

| Case type | Best action | Main goal |

|---|---|---|

| Low-value case, weak proof | Refund fast | Avoid fees and ratio damage |

| High-value case, strong proof | Pursue chargeback representment | Revenue recovery |

| Shipping or billing confusion | Fix the issue and contact the customer | Stop repeats |

The takeaway is simple. Don’t spend an hour defending a case worth less than the fee and staff time. Save that effort for disputes backed by compelling evidence that is clean, timely, and easy to read.

Refund weak cases fast. Fight the ones you can clearly win.

During this window, plug prevention alerts from card networks into your daily process. Mastercard-related alerts may come through Ethoca, while Visa-related cases may route through CDRN or RDR. If you want a plain-language breakdown, this guide on how Ethoca stops chargebacks is worth reading.

This is also where Chargebase can help. Chargebase is chargeback management software built for e-commerce and SaaS businesses. It connects with a payment provider quickly, monitors dispute signals, and sends real-time alerts when a fast refund or rule-based action can stop a chargeback before it becomes formal. It also supports CDRN and RDR, and merchants can apply more than 10 automation rules to handle common cases without slow manual work. Because pricing is pay-per-alert, teams can act without taking on a large fixed-cost tool.

For cases you choose to fight, keep your evidence tight. Pull order details, proof of delivery, tracking information, sales receipt, IP or device data, login history, renewal notices, cancellation logs, and support transcripts. This guide on winning chargebacks is a helpful check on what strong evidence looks like.

Days 21 to 30, automate what works and fix the causes

The last 10 days are about turning good decisions into routine. If the plan still depends on one person remembering every step, it will break during your next sales spike.

Track a small set of numbers every week through your chargeback monitoring program: chargeback ratio, alert save rate, time to first action, win rate by reason code, refund rate after alerts, and duplicate refund errors. That last one matters more than teams think. A rushed process can create a second loss on the same order.

Then review what drove the disputes in the first place. Shorten the cancel path and clarify your refund policy. Clean up the billing descriptor. Send renewal reminders before rebills. Add better order and delivery emails that include OTIF compliance details and ASN transmission logs as proof for shipping-related disputes. Tighten AVS, CVV, or 3DS where fraud is rising. If you need a good benchmark, these tips for keeping chargeback ratios low line up well with what high-volume merchants already do.

Also, stress-test your staffing. If alerts sit untouched on weekends, your process still leaks money. If finance sees a spike but support doesn’t, or your acquiring bank flags delays, your reporting is too slow. A healthy system moves the same way every day, not only when leadership asks for updates.

If you want to compare your setup against broader industry practices, this overview of chargeback management best practices can help spot gaps. Still, the biggest lesson is simpler than most teams expect: chargebacks are often a symptom of weak billing, weak service, or slow response (including friendly fraud from billing confusion), not only fraud.

A good chargeback recovery plan uses automated templates to streamline evidence submission and fixes today’s losses and tomorrow’s causes at the same time. That’s why automation matters. It gives your team speed where speed saves money.

Chargebacks rarely disappear on their own. Build the plan, assign one owner, and start with the first 10 days this week.

You might also want to read

Uncategorized

Apr 10, 2026

Uncategorized

Apr 09, 2026

Uncategorized

Apr 08, 2026

Uncategorized

Apr 07, 2026