Chargeback Time Limits by Card Network, Visa vs Mastercard vs Amex, what merchants can actually rely on

Jan 30, 2026

Chargebacks don’t feel like a fair fight. Your customer can tap “cardholder dispute” in a banking app in seconds, then your team is stuck racing a clock you didn’t start.

The tricky part is that chargeback time limits aren’t one single deadline. There’s the cardholder’s window to file, the merchant’s window to respond with a representment, and extra program rules that can shorten your real timeline, with the fire drill starting on day one of the dispute notification. If you’re running e-commerce or SaaS, knowing what’s stable (and what isn’t) is the difference between a clean representment and an automatic loss.

Why chargeback time limits feel slippery (and why they matter for your chargeback process)

Most merchants ask a simple question: “How long does a customer have to chargeback a transaction?” The real answer is more like: “It depends on the network, reason code, and when the clock starts.”

Across major networks as of January 2026, cardholders often have up to 120 days to file a dispute under the general 120 days network standard. But merchants usually get far less time once the chargeback hits their processor. Common merchant response windows range from about 20 to 45 days, depending on the network and case stage.

Two details make this feel unpredictable:

First, “120 days” doesn’t always mean 120 days from the transaction date. For certain disputes, the clock can start later, such as the delivery date, the date a recurring payment posted, or the date a service was supposed to be provided.

Second, your payment processor or acquiring bank can impose shorter internal cutoffs. Even if the network allows 30 days, your acquiring bank might want your evidence in 10 to 15 days so they can review and forward it on time. If you’ve ever heard “you missed the deadline” and thought “but it’s only day 22,” that’s why.

If you want an easy merchant-friendly refresher on how these windows vary, this overview is a useful starting point: Understanding credit card chargeback time limits across networks.

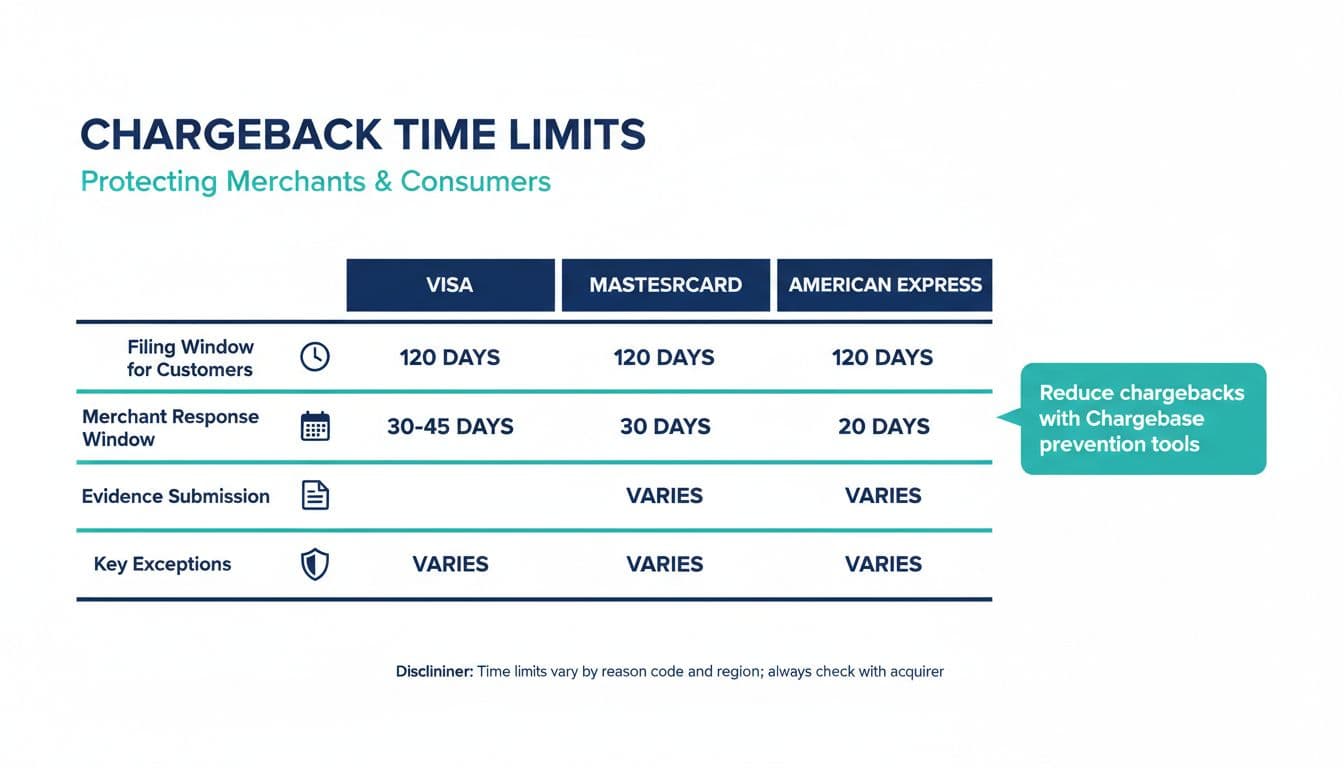

Visa vs Mastercard vs Amex: the time limits merchants should know

At a high level, Visa, Mastercard, and American Express often look similar from far away, while Discover chargeback time limits also follow similar patterns. Up close, their timing rules feel different because of how each network and issuing bank defines the “start date” for a cardholder dispute, and how fast you must react once the dispute enters the system.

Here’s a practical comparison you can share with ops and support teams.

| Card network | cardholder dispute window | merchant response window | What usually changes the clock |

|---|---|---|---|

| Visa | Up to ~120 days | ~30 days (often less at later stages) | Expected delivery date, service date, some fraud scenarios can be shorter |

| Mastercard | Up to ~120 days | ~45 days (can tighten in some steps) | Processing date rules, some reason codes can have shorter filing periods |

| American Express | Up to ~120 days | ~20 days per phase | Statement timing, some dispute types can extend, process can differ from Visa and Mastercard |

Visa chargeback time limits (what to expect in practice)

Visa chargeback time limits commonly allow a filing window up to about 120 days, often counted from the transaction date or the expected delivery date (whichever applies). Some fraud-related scenarios can shorten the effective window.

For merchants, a common response time is about 30 days from notice, and it can shrink in later stages (pre-arbitration can move fast). If you’re trying to win representment with tools like Compelling Evidence 3.0, that means your “real” window is often the time it takes to gather proof plus your processor’s internal cutoff. In other words, it’s rarely a comfortable 30 full days.

For a deeper Visa-specific discussion, this guide provides helpful context: Visa chargeback time limit guide.

Mastercard chargeback time limits (similar headline, different edges)

Mastercard chargeback time limits also tend to land around a 120-day filing window for cardholders, but the chargeback process is strict about how it defines the processing date and certain business dates used in its systems. Some dispute reasons can have shorter filing limits, so “120” is not a guarantee.

Merchants often see around 45 days to respond at common stages, but there can be tighter windows when additional information is requested. The big operational takeaway is that Mastercard can give you more breathing room than Visa at the main representment stage, but you still can’t treat it like a slow-moving process.

American Express chargeback time limits (the one that surprises teams)

American Express chargeback time limits are the network most likely to catch teams off guard because the workflow can feel different from Visa and Mastercard. Cardholders often have up to about 120 days to dispute, and Amex can treat certain categories (such as not received, canceled, or returned goods) differently in how it measures deadlines, including fraudulent transaction claims.

From the merchant side, response timelines are commonly shorter, often around 20 days per phase. That makes speed a bigger factor than perfect documentation. These rules also differ from other platforms like PayPal.

If you want an Amex-focused explanation written for merchants, this is a solid reference: Amex chargeback time limit guide.

What merchants can actually rely on (and what breaks in real life)

Deadlines matter, but operational reality matters more. Here’s what tends to hold up across networks, and where merchants get burned.

You can rely on this: once a chargeback is opened, your time to act is short. Even if the cardholder had up to 120 days, your merchant response is usually weeks, sometimes less. Build your chargeback process like a fire drill, not a research project.

You can’t rely on this: that your acquiring bank will honor the full network window. Many acquiring banks set earlier internal deadlines so they can validate and package your compelling evidence.

You can rely on this: time limits vary by reason code and circumstance. “Not received” disputes often anchor timing to the delivery date. Subscription disputes can tie to billing cycles or cancellation claims.

You can’t rely on this: that you’ll win if you respond. Industry-wide win rates for merchants are not high, and missing even one required document or format requirement can sink the case.

The most dependable approach is to reduce how many disputes become chargebacks in the first place, especially categories like friendly fraud, unauthorized charges, and fraudulent transactions that merchants must defend against to protect their merchant rights. That’s where alert programs and pre-dispute tools come in for effective dispute management. Chargebase’s documentation explains why alerts matter for keeping your ratio under control: effective strategies to keep chargeback rates low. It also helps to understand issuer-alert sources like Ethoca and how merchants use them to act before a dispute turns into a chargeback: how Ethoca Alerts help stop chargebacks early.

Prevention beats deadlines: how Chargebase helps you stop disputes sooner

If chargeback time limits are the clock, prevention tools are how you get ahead of it as your core chargeback management strategy.

Chargebase is a chargeback prevention and recovery platform built for e-commerce and SaaS teams. Instead of waiting for a formal chargeback, it connects to your payment provider in minutes and uses programs like Verifi CDRN and Visa RDR, plus issuer alert networks, to flag disputes early. That dispute management matters because the simplest way to stop many chargebacks is also the least exciting: refund quickly while the case is still in a pre-dispute stage.

A few details that make this practical for busy teams:

- Real-time alerts when they matter, so you can act while the window still exists.

- Automation rules with automated technology for the chargeback process (especially with RDR and CDRN), so common cases can be handled consistently when the 120 days window is still open for the customer.

- Performance-based pricing respecting chargeback time limits, where you pay per alert, not a vague monthly promise. Typical pricing models in these programs are often in the range of about $15 per alert for CDRN or RDR and about $25 per alert for Ethoca, with enrollment times varying by program (hours for some alerts, days for some auto-resolution setups within chargeback time limits).

The point is not to “win” more chargebacks. It’s to keep more cases from ever turning into chargebacks that count against your ratios, drain your team, and trigger monitoring risk.

Conclusion

Visa, Mastercard, and Amex each have their own clocks, but the pattern is consistent: cardholders get months to file a cardholder dispute, merchants get weeks. The only safe way to operate is to treat chargeback time limits as “short by default,” then verify the exact window by reason code and processor rules, since these are key variables that influence the outcome. Failing to act on day one can lead to a loss by default. Chargeback time limits are a backstop, not a guarantee. If you reduce disputes before they become chargebacks through alerts and fast refund decisions, deadlines stop being a constant threat. High-stakes cases can often escalate to arbitration if deadlines are not strictly managed.

You might also want to read

Uncategorized

Apr 10, 2026

Uncategorized

Apr 09, 2026

Uncategorized

Apr 08, 2026

Uncategorized

Apr 07, 2026