Ethoca Consumer Clarity Explained for Merchants in 2026

Mar 23, 2026

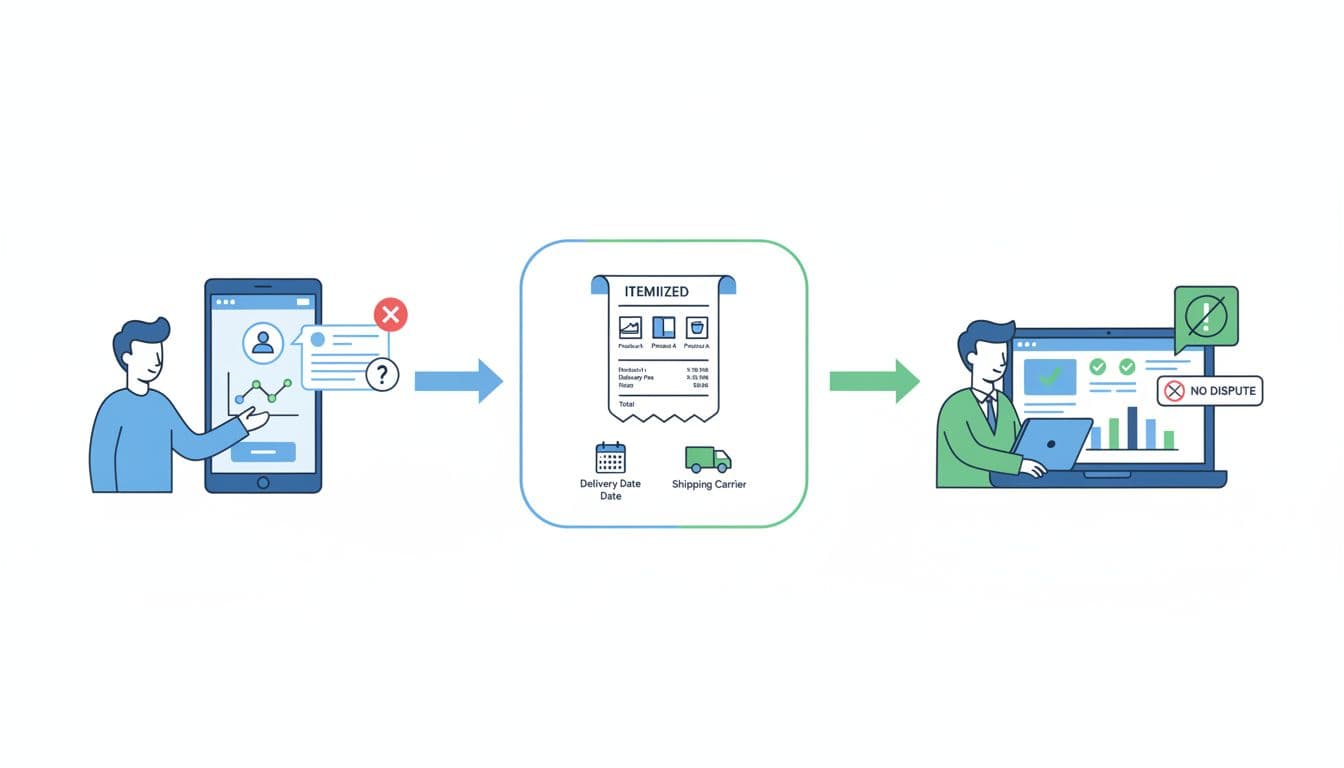

Ever had a customer dispute a charge they actually made? That single moment of confusion can cost a merchant the sale, the product, the fee, and hours of staff time. Ethoca Consumer Clarity tries to stop that before a bank dispute starts.

Instead of showing a shopper a vague billing line, it gives issuers richer purchase details inside banking channels. In crowded payment environments, clarity is often cheaper than fighting later. This guide explains how the system works, why it matters more in 2026, and where Chargebase fits if you want fewer chargebacks overall.

What Ethoca Consumer Clarity actually shows cardholders

Ethoca Consumer Clarity, once known as Ethoca Eliminator, is a Mastercard product built to reduce “I don’t recognize this” disputes. Mastercard’s Consumer Clarity for Merchants documentation describes a setup where banks can show cardholders more context, such as the merchant name, location, contact details, website, and receipt-level data when available.

That matters because many chargebacks start with poor memory, not fraud. A customer sees a strange descriptor, taps the charge in their bank app, and panics. Consumer Clarity replaces that blank space with a better explanation.

Bank service agents benefit too. When a caller asks about a charge, the agent can see richer data instead of a bare transaction line. That makes it easier to steer the customer back to the merchant when the purchase is valid.

Instead of calling the bank to reverse the payment, the customer may recognize the purchase or contact the merchant first. Ethoca has also explained how transaction clarity helps reduce disputes because it gives answers at the exact point of doubt.

Consumer Clarity works before the formal chargeback stage, which is where most merchants want the problem solved.

In practice, think of it like turning a blurry receipt into a labeled package. The bank sees more. The shopper sees more. As a result, the merchant gets fewer accidental disputes. Mastercard says the network reaches more than 145 million merchant locations across 200-plus countries, so this is no longer a small pilot idea.

Why merchants care more about it in 2026

For merchants, the value is simple. Fewer confused shoppers means fewer preventable chargebacks, fewer fees, and less revenue leakage. If you need a quick refresher on the basics, Chargebase has a useful guide for understanding chargebacks.

The biggest win shows up in a few common business models. E-commerce brands cut “item not recognized” disputes. SaaS teams reduce recurring billing confusion. Digital services get fewer first-party fraud claims dressed up as bank complaints. That also protects your chargeback ratio, which processors and card networks watch closely.

Subscriptions stand out in 2026. Ethoca has highlighted more insight and control over subscriptions in digital bank channels, including tools that can help a cardholder manage a recurring service from within a banking app. When people can spot and stop a renewal cleanly, they’re less likely to file a chargeback out of frustration.

That shift also helps finance teams. Lower dispute volume means fewer write-offs, fewer manual cases, and cleaner reporting. Over time, even a small drop in preventable chargebacks can lift margins.

Of course, not every dispute disappears. True fraud still happens. Shipping issues still upset buyers. Yet Consumer Clarity lowers the noise. Your team can spend less time sorting honest confusion and more time fixing real risk.

Consumer Clarity works best with chargeback prevention software

Here’s the catch: Consumer Clarity is not a full chargeback program. It doesn’t replace fraud checks, refund rules, issuer alerts, or representment work. It helps before a dispute starts, but you still need a way to act fast when a real alert arrives.

That’s where Chargebase comes in. Chargebase is chargeback prevention software built to help merchants reduce the number of disputes across card and fintech payment flows. It connects to a payment provider in about two minutes, flags possible chargebacks early, and sends real-time alerts so teams can refund before a case becomes formal.

The platform also supports programs such as Ethoca, RDR, and CDRN. Based on Chargebase’s published details, Ethoca alerts are offered on a pay-per-alert model, around $25 per alert, while RDR and CDRN examples are around $15. RDR can auto-refund with more than 10 automation rules, while Ethoca and CDRN can fit manual review or refund flows.

That mix matters because merchants rarely lose money for one reason alone. Some disputes come from confusion, which Consumer Clarity can ease. Others need early alert handling and fast action. If you want a deeper look at the alert side, Chargebase explains how Ethoca alerts work and shares practical advice on how to keep chargeback rates low.

Used together, clearer transaction data and fast alert automation can help most companies keep more revenue and avoid unnecessary disputes.

Final take

The short version is this: Ethoca Consumer Clarity helps valid purchases look valid before a customer hits the dispute button. For merchants in 2026, that can mean fewer false claims and less wasted effort. Pair it with fast action tools, like Chargebase’s alert and refund workflows, and your odds of stopping chargebacks get much better.

You might also want to read

Uncategorized

Apr 10, 2026

Uncategorized

Apr 09, 2026

Uncategorized

Apr 08, 2026

Uncategorized

Apr 07, 2026