Mastercard Chargeback Reason Codes Cheat Sheet With Evidence By Code (2026)

Mar 05, 2026

Chargebacks feel like getting a parking ticket from the issuing bank for a street you didn’t know had signs. You still have to pay, unless you can prove you were in the right, fast.

This 2026 cheat sheet breaks down the most common Mastercard chargeback reason codes, what they usually mean in plain English, and the best evidence to submit by code. Submitting compelling evidence is the only way to successfully overturn the dispute. It also covers what’s changing as Mastercard continues to consolidate older codes into a smaller set, which affects how you label and fight disputes.

How Mastercard reason codes work in 2026 (and what’s being consolidated)

Mastercard reason codes, used by the issuing bank to define the dispute, tell you why a card transaction was reversed. The code also hints at what evidence can win the case. In practice, it’s like a “case type” label. Pick the right proof for the label and you have a chance. Miss the label’s requirements and you’re arguing the wrong case.

In recent years, Mastercard simplified its catalog into fewer, broader codes (mostly starting with “48”), consolidated under categories such as Point-of-Interaction Error, Cardholder Dispute, and Authorization-Related Chargeback. As of 2026, there aren’t widely announced brand-new codes, but older ones are still being phased out or merged into the main set. For example, some “amount differs” style disputes have been moving under 4834, and several “goods/services” and cancellation flavors increasingly land under 4853 instead of older, narrower codes. That means your team may see fewer unique numbers, yet more variety inside each bucket.

Time limit still matters as much as the facts. A common pattern is that merchants get a limited response window (often around 45 days), while cardholders can have longer to file in certain scenarios (often up to 120 days). Exact deadlines vary by dispute type and region, so confirm the rules for your BIN region and program in Mastercard documentation. Keep the official guide bookmarked, because it’s the source networks and acquirers reference during escalations: Mastercard’s Chargeback Guide (Merchant Edition).

Quick reality check: reason codes are only half the battle. Your operational speed, logs, and refund habits often decide the outcome.

If you’re trying to protect your dispute ratio, it also helps to treat chargebacks as a process problem, not a one-off event. Work with your acquirer, the merchant’s point of contact for documentation. Chargebase’s docs lay out a practical framework for alerts and ratio control in tips to keep chargeback rates low.

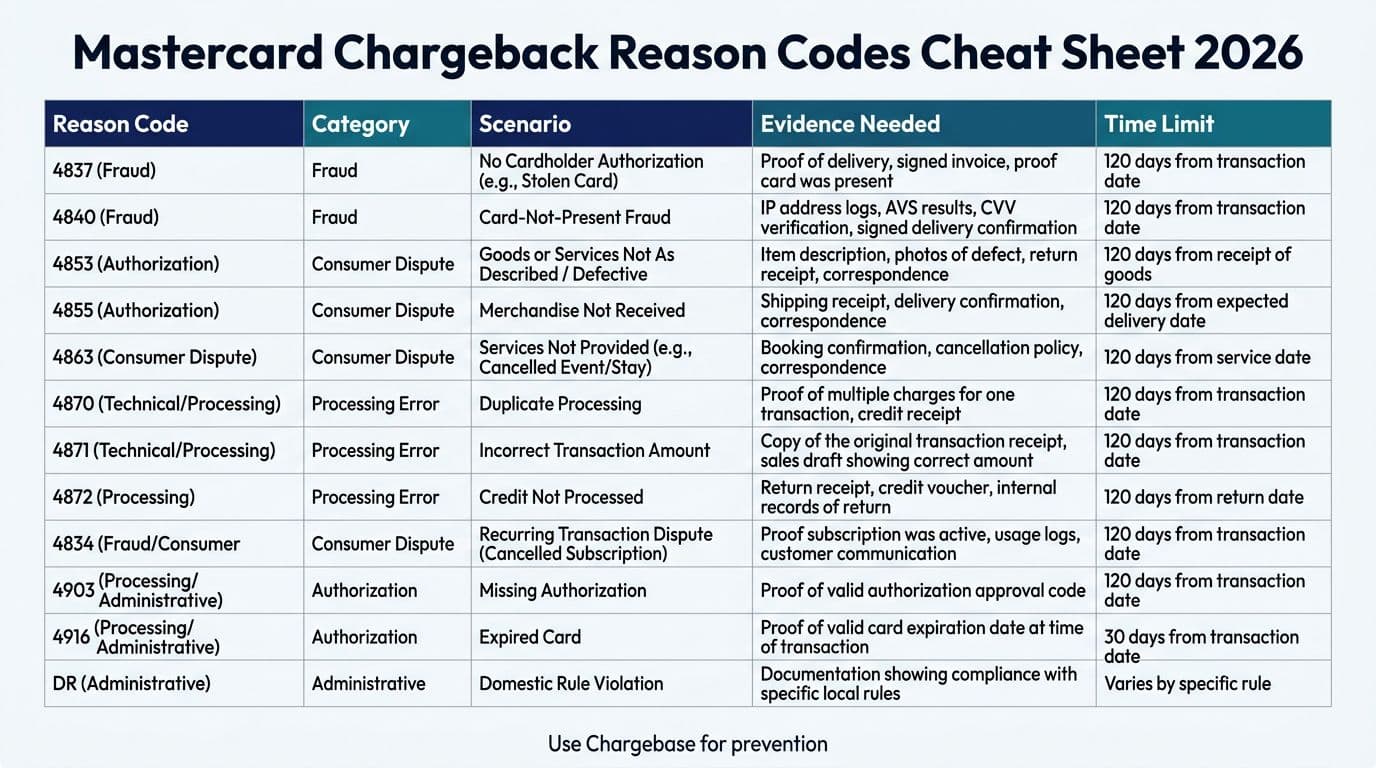

Mastercard chargeback reason codes cheat sheet (2026): evidence by code

Use the table below as a working cheat sheet. Codes and wording can vary by program, so treat it as a “what to pull first” guide, not legal advice.

| Reason code | Usual category | Common scenario | Best evidence to submit | Notes |

|---|---|---|---|---|

| 4837 | Fraud | Reason code 4837: No Cardholder Authorization | SecureCode results (if used), Address Verification Service/CVC2 match, device/IP history, account login trail, delivery proof | Stronger with SecureCode and consistent device signals |

| 4840 | Fraud or processing | Card data used in a suspicious way | Transaction logs, 3DS/AVS/CVV, velocity checks, customer history | Show why the order looked legitimate at the time |

| 4863 | Cardholder doesn’t recognize | No Cardholder Authorization | Descriptor evidence, email receipts, account access logs, prior successful purchases | Often “friendly fraud” or billing descriptor confusion |

| 4870 | EMV chip liability | EMV liability shift | Terminal data, EMV tags, proof of chip read or why fallback occurred | POS merchants should retain EMV data fields |

| 4871 | EMV chip/PIN liability | Chip liability shift | PIN-capable terminal proof, EMV tags, transaction certification | Issuer may push liability to the merchant in some cases |

| 4808 | Authorization or processing error | Reason code 4808: No valid auth, wrong account, data issues | Auth approval code, gateway/acquirer logs, time stamps, correction documentation | Some older “account” codes are being routed here |

| 4834 | Processing/amount dispute | Reason code 4834: Duplicate processing, amount differs, paid by other means | Itemized invoice, receipt, batch and clearing records, cancellation or adjustment proof | Helpful when you show exact math and timelines |

| 4853 | Cardholder dispute (broad) | Reason code 4853: Counterfeit merchandise, digital goods, not as described, canceled, returned, services complaint | Terms accepted, return policy, support tickets, delivery/usage logs, signed agreements | A catch-all code that absorbs older sub-types |

| 4860 | Credit not processed | Refund promised but not received | Refund transaction ID, refund date, processor confirmation, policy screenshots, support thread | Also explain refund timing expectations clearly |

| 4801 | Documentation request | Issuer asked for transaction info | Transaction receipts, invoice, order record, customer comms | Treat like a “retrieval” sprint, not a fight |

| 4802 | Illegible/missing info | Docs provided but incomplete | Clean copies of receipts, full order details, clear customer identifiers | Resubmit in a readable, complete bundle |

| 4916 | Non-receipt | Goods or services not provided | Carrier tracking, delivery confirmation, address match, shipment weight, claims history | Add replacement/refund timeline if you offered it |

| 4903 | Merchant dispute handling | Related to dispute processing rules | Complete case file, acquirer guidance, proof you met program requirements | Confirm requirements with your acquirer first |

Two patterns to remember:

- Fraud codes lacking cardholder authorization (like 4837) reward technical proof (SecureCode, Address Verification Service/CVC2, device data, EMV fields).

- Cardholder Dispute codes (often 4853, 4860, 4916) reward “customer journey” proof (policies, support, delivery, usage, cancellation).

For a broader list and cross-references, compare your cases to a current catalog like Chargebacks911’s Mastercard reason code list. It’s useful for sanity checks when an issuer’s description feels vague.

Turning reason codes into fewer chargebacks (and how Chargebase helps)

If your team only reacts after the chargeback posts, you’re already in the expensive phase. A better approach is to tie each reason code family to one of two actions: prevent it early (like verifying cardholder authorization), or prepare evidence automatically.

Start with a simple rule: when you see a dispute alert and the order is low margin, refund early. That single habit often cuts loss rate and ops time, avoiding the complex Representment process. The trick is doing it consistently, with checks that prevent double refunds and repeat abuse, especially in high-risk areas like recurring transactions.

That’s where Chargebase fits. Chargebase is chargeback prevention and recovery software built for merchants who accept card payments through gateways and fintech stacks. It connects to your acquirer quickly (often without code) and then helps you act before a dispute becomes a network chargeback. In other words, it turns “surprise chargeback mail” into an early heads-up you can handle while it’s still fixable.

Chargebase supports major dispute prevention channels, including Ethoca alerts and programs like RDR and CDRN, and it uses automation rules plus real-time alerts so your team isn’t stuck triaging every case manually. Alerts can trigger for errors like late presentment and fraudulent processing. Pricing is performance-based (pay per alert), which keeps incentives aligned. In the product details shared, example pay-per-alert pricing includes around $25 per Ethoca alert and $15 per alert for programs like RDR and CDRN, with enrollment times that can range from hours to several days depending on the network. Some flows support manual refunds, while others are built for auto-refunds only, so your playbook should match your risk tolerance.

If you want to understand one of the major alert networks more clearly, see Chargebase’s explainer on Ethoca for chargeback prevention. Also, for additional context on how reason codes connect to real merchant workflows, this 2026 overview is a helpful companion: chargeback reason codes explained with examples.

The best “evidence” is the evidence you never have to submit, because you prevented the chargeback upstream.

Conclusion

Mastercard chargeback reason codes guide your defense by telling you what to prove, and the time limit you have to prove it. In 2026, broader codes (especially Reason code 4853, a major Cardholder Dispute bucket) mean your evidence quality matters more than the label’s wording. Build templates for fraud, non-receipt, and refund disputes, then respond inside the deadline every time. If you also add prevention through alerts and automation, you can shrink your chargeback volume instead of just arguing about it. The goal isn’t perfect representment, it’s fewer disputes and more revenue kept by maintaining cardholder authorization records.

You might also want to read

Uncategorized

Apr 10, 2026

Uncategorized

Apr 09, 2026

Uncategorized

Apr 08, 2026

Uncategorized

Apr 07, 2026