How Network Tokenization Cuts Fraud and Chargebacks

May 08, 2026

Every credential on file, such as a primary account number, is a liability. If that credential gets stolen, one bad transaction can turn into lost goods, dispute fees, and a chargeback ratio that keeps climbing.

That is why more merchants are moving to network tokenization. It swaps the real card number for a network-issued token, which is far less useful to criminals and easier for issuers to trust. A payment service provider can help facilitate this transition.

For companies that take card payments online, this change can enhance the checkout experience, lower fraud, and reduce the chargebacks that come after it.

Key Takeaways

- Network tokenization replaces primary account numbers with secure, network-issued tokens that are merchant-specific, domain-restricted, and far harder for criminals to reuse across breaches.

- It boosts issuer trust with richer assurance data and cryptograms, delivering 2-6% higher authorization rates and fraud reductions of 18-60% depending on the merchant profile.

- Chargebacks drop directly from fewer successful fraud transactions and indirectly from smoother recurring billing via card account updater integration.

- For best results, pair network tokens with alert networks like Ethoca and Verifi to handle post-authorization disputes before they formalize.

What network tokenization changes at checkout

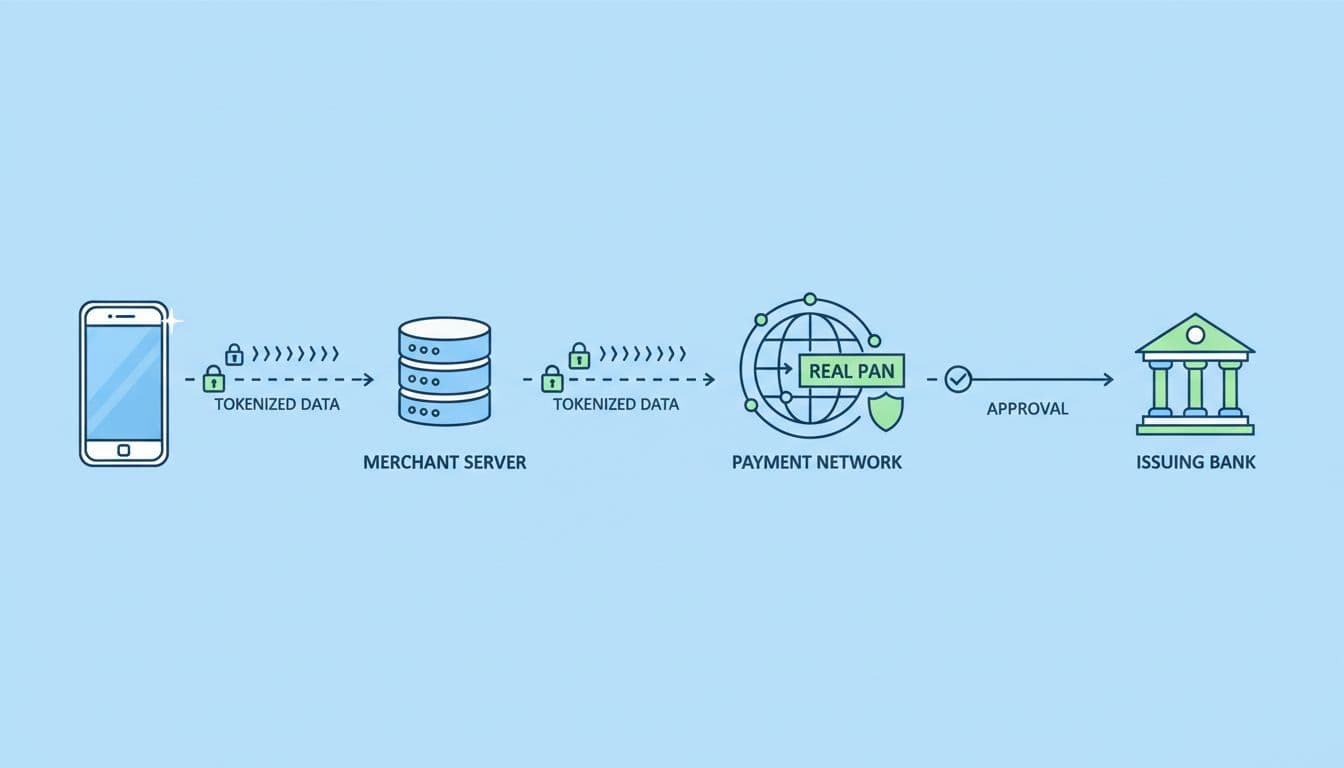

Network tokenization replaces the card’s primary account number with a substitute value issued by the card networks, such as Visa or Mastercard. Through token provisioning, the merchant receives and keeps the token, not the raw primary account number. When a payment runs, the card networks map that token back to the real account in a protected environment.

That sounds similar to ordinary tokenization, but there is an important difference. A gateway or payment vault token usually works inside one processor’s system or acquirer’s setup. A network token is tied to the card networks themselves, adhering to EMVCo standards, and it often carries extra data that helps the issuer judge the payment more accurately.

In many cases, the token is also merchant-specific, linked to a particular merchant, device, or use case. That matters because stolen data becomes much harder to reuse somewhere else. A fraudster who gets the token usually cannot spend it the way they could spend a plain card number.

This quick comparison shows why merchants care about the difference:

| Payment setup | What gets stored | If data is stolen | Issuer confidence & authorization rates |

|---|---|---|---|

| Raw card on file | Actual card number | High misuse risk | Lower |

| Gateway token only | Processor-specific token | Better than raw PAN, but limited | Varies |

| Network token | Network-issued token plus token data | Much harder to reuse | Often higher |

Another benefit shows up in recurring billing, smoothing the checkout experience for returning customers. When a customer gets a new plastic card because the old one expired or was replaced, network tokenization integrates with card account updater services for seamless updates. That means fewer failed renewals, fewer customer service issues, and fewer awkward cases where a customer sees multiple retries and disputes the charge later.

Published payment industry summaries, including Orchestra Solutions on network tokens and Solidgate’s breakdown of business benefits, point to the same pattern: safer credentials, better approval rates, and less exposure when card data is compromised.

Why fraud drops when the real card number disappears

Most online payment fraud still happens in card-not-present channels. Recent 2026 benchmark data puts the average overall chargeback rate near 0.26%, while many online merchants sit closer to 0.6% to 1%. At the same time, card-not-present fraud keeps rising because attackers don’t need the physical card. They only need usable credentials.

Network tokenization makes those credentials much less useful.

First, network tokenization limits the value of stolen data from data breaches. If an attacker breaches a merchant database and finds only network tokens, the haul is weaker than a list of raw card numbers. Those domain-restricted tokens do not travel well outside the intended environment.

Second, network tokenization improves transaction-level trust. Tokenized payments can include a single-use cryptogram and richer token assurance data like the token requestor identifier. Issuers get a clearer signal that the transaction came through an approved path. As a result, they can approve more good payments and reject suspicious ones with greater confidence.

That second point matters more than many merchants expect. Fraud tools often create a tradeoff between blocking bad orders and declining good ones. Better payment data softens that tradeoff. Several providers report an authorization lift of roughly 2% to 6% when network tokens replace stored PANs. Fraud reduction figures vary by merchant profile, but public claims in the market often land between 18% and 60%, as shown in Oceanpayment’s review of token-based approvals and the sources above.

The gains won’t look the same for every business. A subscription app with saved cards will see one pattern. A high-ticket retailer shipping physical goods will see another. Still, the main effect is consistent: fewer exposed credentials means fewer stolen-card purchases in the first place.

How lower fraud turns into fewer chargebacks

The direct link is simple. Network tokenization ensures fewer criminals can place orders with stolen cards, so fewer cardholders will file fraud disputes. That alone can remove a meaningful slice of chargebacks for merchants with high third-party fraud.

The indirect link is just as useful. Better issuer trust leads to cleaner approvals and higher authorization rates. Cleaner approvals mean less manual review, fewer strange retries, and fewer cases where customers see activity that looks suspicious. In subscription models, network tokenization’s lifecycle management also reduces failed rebills and card-refresh problems in recurring payments, which can cut the confusion that often sparks disputes.

There is a strong margin angle here as well. Recent fraud and dispute estimates show merchants can lose about $4.61 for every $1 of fraud once fees, lost goods, shipping, and labor are counted. A lower fraud rate protects more than revenue. It also protects staff time and card network standing, while enabling payment optimization.

Yet tokenization has limits. It does not fix late delivery. It does not make a vague billing descriptor clearer. It does not stop a customer from saying “I forgot that renewal” or “I did not authorize this” after using the service. Friendly fraud still makes up a large share of disputes, and it is rising in many sectors.

That is why network tokenization should be seen as a front-line defense, not a complete chargeback strategy. It removes a large class of payment risk at the credential level. It does not solve every post-purchase dispute.

For a broader view of how tokenization affects fraud, approval rates, and payment performance, Spreedly’s tokenization paper is a useful reference.

Why tokenization works best with alerts and automation

Once you accept that tokenization does not stop every dispute, the next step becomes clear. You need a way to catch pre-chargebacks after the customer contacts the bank.

That is where alert networks and automated workflows matter. Programs like Ethoca, Verifi CDRN, and Verifi RDR can warn merchants early or resolve eligible cases before a formal chargeback is created, as data flows from issuers through acquirers. If you want a quick primer, Chargebase has a helpful page on Ethoca alerts overview and a clear explanation of Verifi CDRN alerts.

Network tokenization protects the credential. Chargeback alerts protect the transaction after the customer talks to the bank.

This is where Chargebase fits well for many merchants. Chargebase is chargeback prevention software built for e-commerce and SaaS companies that want fewer disputes without adding more manual work. It connects with payment service providers, detects likely chargebacks, and sends real-time alerts when a merchant can still act in time. The workflow is simple: connect, detect, then prevent.

The platform also supports automated handling. Merchants can set more than 10 rules for how disputes should be handled, and RDR can auto-refund eligible cases. Ethoca and CDRN help teams act within short windows before a network chargeback lands. Because pricing is pay-per-alert, costs stay tied to cases where the tool can help.

That combination matters. Network tokenization lowers stolen-card fraud at authorization and simplifies PCI compliance for merchants while boosting authorization rates. Chargebase helps reduce the disputes that still appear after the sale, including many first-party misuse cases that tokenization will never block on its own. If your goal is to keep chargeback rates low, both layers belong in the same plan.

Frequently Asked Questions

What is network tokenization?

Network tokenization swaps a card’s primary account number for a substitute token issued by networks like Visa or Mastercard. Merchants store and use the token, which the network maps back to the real PAN in a secure environment. This follows EMVCo standards and often includes extra data for better issuer decisions.

How does network tokenization differ from gateway tokenization?

Gateway tokens are limited to a single processor or acquirer ecosystem, while network tokens are standardized across card networks. Network tokens are typically merchant- or device-specific, reducing reuse risk, and carry assurance data that improves authorization rates. The result is stronger fraud protection and portability.

Why does it reduce fraud and improve approvals?

Stolen network tokens have low value outside their domain, limiting breach impacts. They provide issuers with token requestor IDs and cryptograms for clearer transaction signals, softening the fraud detection tradeoff. Providers report 2-6% auth lifts and 18-60% fraud drops.

Does network tokenization eliminate chargebacks?

It cuts chargebacks from stolen-card fraud and failed recurring payments, but not friendly fraud or post-purchase disputes. Better approvals reduce suspicious activity that sparks claims. Use it as a front-line defense alongside alerts like Ethoca or Verifi CDRN.

How can merchants implement network tokenization?

Partner with a payment service provider that supports token provisioning and card account updaters. Store tokens instead of PANs to simplify PCI compliance. Combine with chargeback automation for comprehensive protection against fraud and disputes.

The safest card number is the one you never store

Network tokenization reduces fraud because it takes away the raw credential that criminals want most, such as those powering digital wallets. It also gives issuers better data, which can improve approvals and cut the fraud disputes that drive chargebacks, all with minimal latency to avoid slowing transactions.

For merchants, that is the real takeaway. Use network tokens to reduce credential risk, then pair them with alert-driven chargeback prevention managed through an orchestration layer by card networks for stored credentials, so the remaining disputes do not turn into losses. Higher trust transactions from this strategy can also lower interchange costs. When those two layers work together, chargebacks usually fall for the right reasons.

You might also want to read

Uncategorized

Jun 07, 2026

Uncategorized

Jun 06, 2026

Manual vs. Automated Processes

Jun 05, 2026

Uncategorized

Jun 04, 2026