Processing Error Chargebacks in 2026, the 9 Checkout Mistakes That Trigger Disputes (Duplicate Charges, Wrong Amount, Currency Confusion)

Feb 12, 2026

A customer hits “Pay,” sees a confirmation, and moves on. Then their Issuing Bank app shows something that looks off, a duplicate, the wrong amount, a weird currency, and they tap “Dispute” before they ever message support. That’s how processing error chargebacks often happen: not because the customer wants to cause trouble, but because the checkout experience left room for doubt.

In 2026, disputes feel faster and more casual. Issuers keep making it easier for cardholders to question a transaction, and volume of Card-Not-Present Transactions keeps climbing across the industry. Even if fraud gets most of the headlines, processing mistakes still create expensive, avoidable chargebacks, plus fees, time, and risk to your chargeback ratio.

This guide breaks down the nine checkout errors that most commonly trigger Merchant Error Chargebacks, and what to fix in your Payment Processing so fewer payments turn into problems.

Why processing error chargebacks hurt more in 2026

The complexity of the Dispute Process makes processing errors particularly frustrating because they often look obvious to the cardholder. If someone thinks they were charged twice, they don’t assume it’s a settlement timing issue. They assume you took their money twice. Same with currency: a shopper in Europe who sees a USD amount (plus FX impact) might not read the fine print, they just see a number that doesn’t match what they expected.

There’s also a practical problem: processing error disputes are hard to “win”. If your logs, receipts, and gateway records don’t line up cleanly, Issuing Banks tend to side with the cardholder. And if a case escalates, the process can get more expensive. Stripe’s overview of how chargeback arbitration works across card networks is a good reminder that once a dispute reaches later stages, the cost in effort and fees rises quickly.

What’s changed recently is the mix of disputes. Many industry projections still point to overall chargebacks increasing through 2026, while a large share are considered “invalid” or “Friendly Fraud.” That doesn’t reduce the damage from merchant mistakes, it makes accuracy even more important. When issuers already expect high dispute volume, you want your checkout records to be boring, consistent, and easy to verify.

Finally, processing error chargebacks often cluster around releases: a new pricing test, a tax update, a subscription migration, Late Presentment, or a payments routing change. If the customer experience is your storefront, then checkout is the cash register in Payment Processing. A tiny misconfiguration can echo across thousands of orders, making Chargeback Prevention essential.

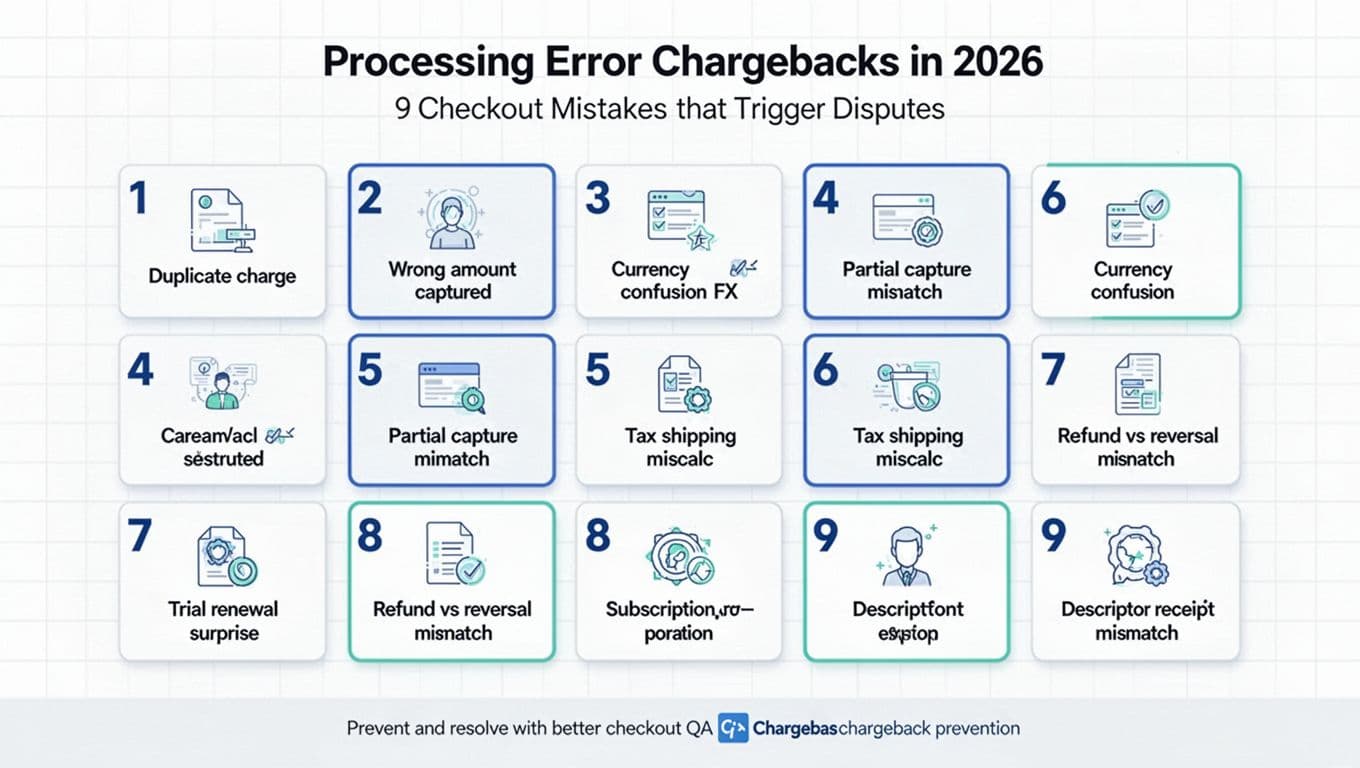

The 9 checkout mistakes that trigger disputes (and what customers see)

Here’s the pattern to watch for: the customer sees one thing at checkout, their bank statement shows another, and the gap creates distrust. Chargeback Reason Codes vary by network, but processing errors usually fall into “duplicate,” “incorrect amount,” “credit not processed,” or similar buckets. For a quick refresher on how Chargeback Reason Codes group together, see Rapyd’s guide to chargeback reason code categories.

| Checkout mistake | What the customer thinks | What to verify first |

|---|---|---|

| Duplicate charge | “They charged me twice.” | Duplicate Processing |

| Wrong amount captured | “That’s not what I agreed to.” | Incorrect Transaction Amount |

| Currency confusion (FX) | “The price changed.” | Dynamic Currency Conversion |

1) Duplicate Processing (usually retries, timeouts, or double capture)

Duplicates often come from a checkout retry after a slow response, a “back button” resubmit, or a payment method that creates multiple authorizations. From the customer’s view, none of that matters. They see two lines on their statement. This scenario aligns with specific Chargeback Reason Codes for duplicate processing.

Your fix is less about support scripts and more about engineering hygiene: enforce idempotency, block double capture, and make “payment pending” states clear so customers don’t re-submit.

2) Wrong amount captured (discounts, shipping, tips, rounding)

This one triggers fast disputes because it feels like a broken promise. It can also be self-inflicted: a promo applies on the cart page but not the final confirmation, a shipping quote changes after address validation, or a tip defaults to a higher value than expected. Always check the Transaction Receipt for accuracy to avoid Incorrect Transaction Amount claims.

The most effective change is simple: show a final itemized total right before confirmation, then email the same breakdown in the receipt so the customer can match it later.

3) Dynamic Currency Conversion and “I paid in my currency… right?”

Multi-currency checkouts fail when the site displays a local currency estimate but the charge settles in another currency. Even if you show a currency selector, the customer may not notice. The dispute shows up as “incorrect amount,” but the root cause is clarity. These issues tie directly to Chargeback Reason Codes related to Dynamic Currency Conversion.

If you sell internationally, be explicit about (1) the transaction currency, (2) whether the bank may add FX fees, and (3) the exact number that will appear on the statement.

4) Partial capture mismatch (split shipments, backorders, or delayed capture)

Partial capture is normal in some models, but it’s a dispute magnet when messaging is weak. The shopper expects one total charge. You capture two smaller amounts as items ship.

If you must split captures, set expectations early and repeat them in order updates. Your receipt should show what shipped, what’s pending, and what each capture represents.

5) Tax or shipping miscalculation (especially after address changes)

Taxes change with location, product type, and exemptions. Shipping changes with carrier rules, surcharges, and delivery speed. The mistake happens when the checkout recalculates late and the customer doesn’t notice, or when your confirmation email shows a different total than the on-site confirmation. Point-of-Interaction Errors or Manual Entry Errors often underlie these tax miscalculations.

Run QA on edge cases: PO boxes, international addresses, VAT inclusive vs exclusive display, and tax rounding across multiple items.

6) Trial or renewal surprise (the “processing error” that looks like deception)

A renewal dispute often gets filed as “I didn’t authorize this,” even when the user technically did. If the trial converts quietly, or renewal notices are inconsistent, banks won’t care that your terms were somewhere on the page. Clear Subscription Auto-Renewal Terms and a prominent Clickwrap Agreement help prevent these authorization disputes under relevant Chargeback Reason Codes.

Make trial conversion and renewal dates unmissable, and keep cancellation simple. If you want a clean mental model for dispute sources, Stripe’s explanation of three types of chargebacks helps separate fraud, service issues, and “I didn’t mean to pay” situations.

7) Refund vs reversal mismatch (customer expects instant, sees nothing)

Customers hear “refund” and expect the charge to disappear immediately. In reality, they may see a pending charge drop off (Transaction Reversal) or a posted charge with a later credit (refund). If you tell them one thing and their bank shows another, they dispute.

Make your support and automated emails precise: “We’ve issued a refund, it can take X business days to post,” and include the amount and last four digits. Stripe’s documentation on handling refunds and disputes is a useful reference if you run a platform or marketplace where timing and ownership can get confusing.

8) Subscription proration errors (mid-cycle plan changes)

Proration is where “math” becomes “emotion.” If a customer upgrades, downgrades, pauses, or changes seats, the resulting charge needs to be easy to predict. If the invoice shows multiple line items that don’t match what they saw on screen, they’ll assume it’s wrong and file Cardholder Disputes.

Your best defense is a clear “today you pay” preview at the moment of change, plus an invoice that mirrors the preview language.

9) Descriptor and receipt mismatch (they don’t recognize you)

A clean checkout can still end in a dispute if the Billing Descriptors on the card statement don’t match your brand, product name, or receipt. This is common when a parent company, processor descriptor, or old DBA shows up instead, leading to Unauthorized Transactions complaints.

Match your Billing Descriptors to your storefront name, keep receipts consistent, and include a short “statement descriptor” line in the confirmation email.

A practical prevention plan (plus where Chargebase fits)

Start with checkout QA and a clear Refund Policy, but don’t stop there. Chargeback Prevention is a system, not a single fix.

First, tighten your internal checks: reconcile auths vs captures daily, flag duplicate transaction IDs, and monitor spikes after deployments. Second, reduce confusion for humans: show final totals clearly, send receipts that match the statement, and explain currency and refund timing in plain language.

Third, assume disputes will still happen and build for early resolution with Fraud Prevention Tools. Chargeback alerts exist because waiting for a formal chargeback is usually too late. When you can act during the alert window, the cheapest “win” is often a quick refund that stops the dispute from becoming a chargeback.

Chargebase is built for that workflow. It’s a Chargeback Prevention and recovery platform for e-commerce and SaaS businesses that connects to your payment provider with a no-code setup (often in minutes), then uses networks like Ethoca, Verifi CDRN, and Visa Rapid Dispute Resolution to detect and prevent disputes before they turn into chargebacks. It supports representment with compelling evidence like proof of delivery, helps follow Visa Core Rules and Visa Compelling Evidence 3.0, sends real-time alerts routed to the issuing bank only when they can help, and uses pay-per-alert pricing so costs track outcomes. Chargebase also aids recovery through tools like the Rebuttal Letter for payment processing disputes. If you want to understand the alert layer better, Chargebase’s guide to how Ethoca helps prevent chargebacks explains why speed matters.

Keeping your ratio low is the other side of the same coin. Chargebase’s documentation on how to keep chargeback rates low outlines what to measure (like time to first action) and how to avoid avoidable mistakes like double-refunding in payment processing.

Conclusion

Merchant Error Chargebacks don’t feel mysterious once you map them back to checkout reality: two different versions of the truth, one in your system, one on the customer’s statement. These are avoidable through better checkout logic. Fix the nine triggers above, and you’ll cut disputes that never should’ve existed.

If you’re already doing the basics, the next step is response speed. The faster you see a Cardholder Dispute forming, the more options you have to stop it before it becomes a chargeback. In 2026, that early window along with Payment Processing efficiency is key to long-term success. Chargeback Prevention remains a continuous system.

You might also want to read

Uncategorized

Apr 10, 2026

Uncategorized

Apr 09, 2026

Uncategorized

Apr 08, 2026

Uncategorized

Apr 07, 2026