Alert Timing Windows For Verifi And Ethoca Programs: A 2026 Guide

Mar 15, 2026

If you accept card payments, Verifi Ethoca alert timing is one of those details that decides whether you save a dispute or eat a chargeback fee.

Think of alerts like a smoke alarm. You don’t have time to “get to it later.” You have a short window to act, usually by refunding, canceling fulfillment, or fixing an account issue. Miss that window and the charge often becomes a formal chargeback that hits your ratios and creates more work.

Below is a practical guide to the timing windows merchants typically see in Verifi and Ethoca programs as of March 2026, plus how to build a response process that actually meets those deadlines.

What an “alert timing window” really means for merchants

A chargeback alert is a pre-dispute signal from participating issuers (the cardholder’s bank) that a cardholder has raised a problem. The alert gives you a short response period to resolve the issue before it becomes a network chargeback.

This timing window matters because it changes the economics. Inside the window, a refund is usually cheaper than a chargeback (fees, lost goods, staff time, and future risk). Outside the window, you’re stuck reacting.

Most merchants run into two timing realities:

- The clock starts fast: Alerts often arrive near real-time, not “end of day.”

- Weekends still count: If your team only handles alerts Monday to Friday, you’ll lose avoidable cases.

If you want a merchant-friendly explanation of why speed is everything, see chargeback alert response windows explained. The big theme is simple: the window is short by design, because banks want quick outcomes for cardholders.

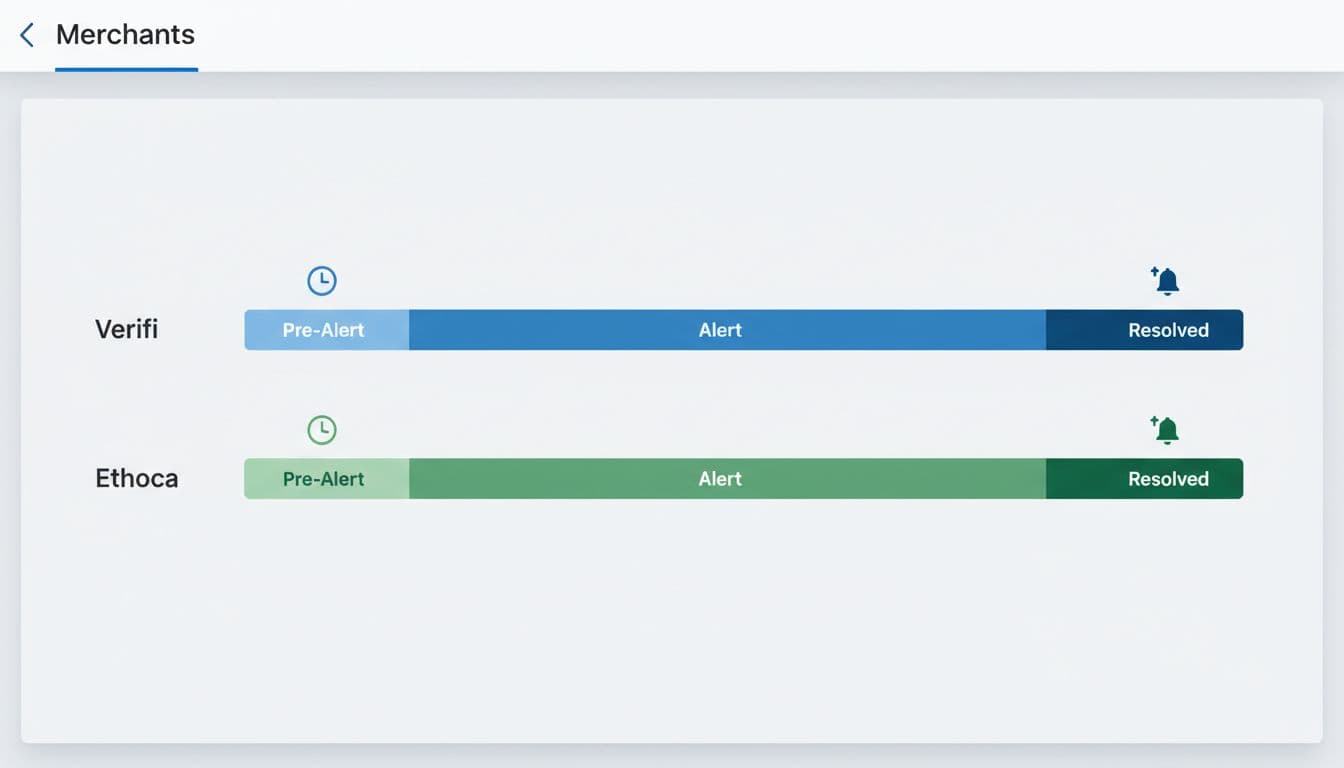

Verifi programs: typical timing windows for CDRN and what changes with RDR

Verifi (a Visa company) runs multiple dispute prevention tools. Two common ones are CDRN (Cardholder Dispute Resolution Network) and RDR (Rapid Dispute Resolution). They behave differently, so timing feels different too.

Here’s the timing most merchants plan around as of March 2026:

- Verifi CDRN: Commonly up to 72 hours to respond. That window is often enough to confirm the order, check fulfillment, then refund (or otherwise resolve) without panic.

- Visa RDR: Instead of “review then decide,” RDR is rules-based. If a case matches your configured rules, it can resolve automatically, usually by refunding. Timing becomes less about human speed and more about having the right rules in place before disputes happen.

This quick comparison helps set expectations:

| Program | Typical response window | Common resolution style | What to plan for |

|---|---|---|---|

| Verifi CDRN | Up to 72 hours | Manual review or manual refund | Fast matching and consistent playbooks |

| Visa RDR | Rules-based (auto-handled when eligible) | Auto-refund only (in most setups) | Good rules, refund controls, and monitoring |

RDR is powerful when your business can confidently auto-refund certain dispute types (for example, low-value orders, clear subscription confusion, or shipments that never left the warehouse). On the other hand, if you sell high-ticket goods, you may want tighter eligibility rules so you don’t refund cases you could have solved another way.

For a simple breakdown of when RDR vs alerts make sense, see Verifi RDR vs Ethoca Alerts vs Order Insight.

Ethoca Alerts: why the window feels tighter (and how to staff for it)

Ethoca (owned by Mastercard) is widely used for near real-time dispute alerts across many markets. The tradeoff is timing pressure.

As of March 2026, merchants commonly see:

- Ethoca Alerts: 24 to 48 hours to act, with many setups treating 24 hours as strict.

That tighter window changes how you work. You can’t rely on a once-a-day queue. You need alerts routed to the right place instantly, plus a response path that doesn’t stall on internal approval.

Ethoca is also often described as strong for broad issuer coverage, especially for merchants selling internationally. Coverage varies by region and issuer participation, but the practical takeaway is that many global merchants run Ethoca alongside Verifi programs to catch more disputes earlier.

A good overview of how Verifi alerts and Ethoca alerts compare is in this guide to Verifi alerts and Ethoca alerts. It reinforces a key point: alerts don’t eliminate disputes, they give you a short chance to choose the outcome.

If you want a plain-language explanation of how Ethoca helps prevent chargebacks, see what Ethoca is and how it helps prevent chargebacks.

Treat Ethoca like an urgent support channel, not a back-office report. If it waits in a shared inbox, the window will close.

How to hit alert windows consistently (without burning out your team)

Timing windows aren’t hard because the actions are complex. They’re hard because they’re time-bound. The fix is a mix of automation, clear rules, and refund controls.

This is where chargeback prevention software helps. Chargebase, for example, is built to reduce chargebacks by connecting to your payment provider quickly (often in minutes), then sending real-time alerts so you can refund early and stop disputes before they become chargebacks. The platform supports official network programs and focuses on automation and pay-per-alert pricing, so costs stay tied to outcomes.

A practical operating model looks like this:

First, decide what you’ll auto-handle. Many merchants create rules like “auto-refund subscription disputes under $X” or “auto-refund if the order hasn’t shipped.” With Visa RDR, Chargebase supports multiple automation rules so eligible cases can resolve without human delay.

Next, make manual decisions fast. For alerts you review, set a simple SLA like “first action in 30 minutes.” That “action” might be pulling the order, stopping fulfillment, or issuing the refund.

Then, prevent double refunds. Alerts often lead to quick refunds, but teams still need checks to avoid refunding twice (for example, if support already refunded, or if an RDR rule triggers). Good workflows block a second refund on the same transaction ID.

Finally, track three metrics that tie directly to timing:

- Time to first action

- Alert acceptance and resolution rate

- Alerts that still become chargebacks

Chargebase also uses performance-based pricing (pay per alert) across common programs, such as Ethoca alerts priced per alert, and Verifi programs like RDR and CDRN priced per alert in many setups. Enrollment timing varies by program, with some enrollments completing in hours, while others can take days, so it’s worth planning ahead before peak seasons.

For more on keeping disputes from counting against your ratios, see how alerts help keep chargeback rates low.

Conclusion

Verifi and Ethoca both buy you time, but the timing windows aren’t equal. CDRN often gives more breathing room (commonly up to 72 hours), while Ethoca frequently demands action inside 24 hours. RDR shifts the problem again by resolving eligible disputes automatically, which makes rule quality more important than staff speed.

If you want fewer chargebacks, build your process around the clock, not around your calendar, then automate the parts you already feel confident about. The best alert program is the one you can run every day, even on weekends, with consistent outcomes.

You might also want to read

Uncategorized

Apr 10, 2026

Uncategorized

Apr 09, 2026

Uncategorized

Apr 08, 2026

Uncategorized

Apr 07, 2026