ACH Return Codes vs Chargebacks for Subscription Merchants

Apr 27, 2026

A failed bank debit and a card dispute can both drain recurring revenue, but they aren’t the same problem.

Subscription teams often group ACH return codes and chargebacks together because both end with lost cash and support work. Yet each one follows a different set of rules, timelines, and recovery options. If you bill through cards and bank debits, you need two separate playbooks.

Why subscriptions trigger both issues

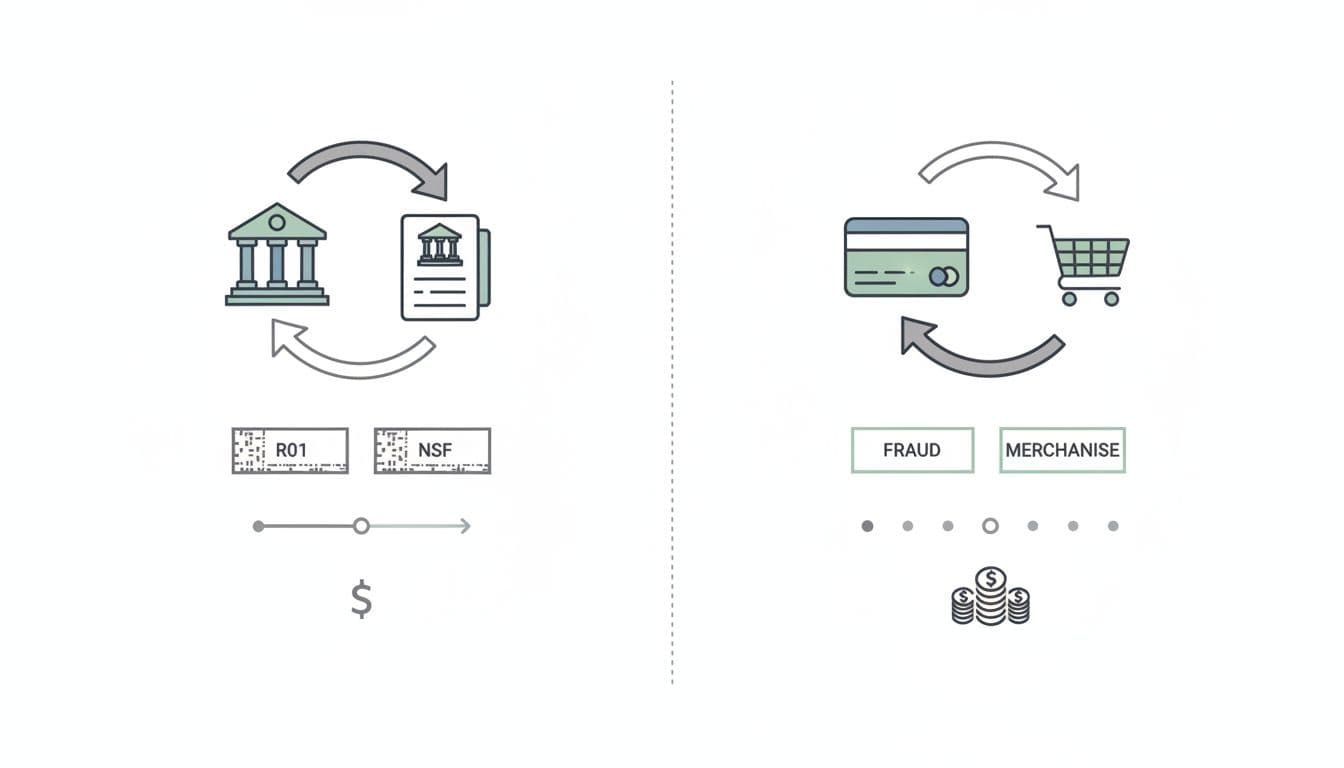

An ACH return happens when a bank debit fails or gets sent back through the network. The return code tells you why. R01 means insufficient funds, R02 means the account is closed, R03 means no account, and R10 points to an unauthorized debit. A practical guide to ACH return codes shows how many codes exist, but subscription merchants usually see the same few again and again.

That coded feedback shapes the next move. A soft failure like R01 may call for a retry after notice to the customer. A hard failure like R02 or R03 usually means you need fresh bank details before the next billing date.

Card chargebacks work differently. The customer disputes a credit or debit card payment through the issuing bank, and the bank pulls the funds back while the case moves through card-network rules. For subscriptions, that often starts with a forgotten renewal, an unclear billing descriptor, a weak cancellation flow, or a customer who goes to the bank before support. Recent 2026 benchmarks still put subscription chargeback rates around 0.5% to 1.0%, which is high enough to pressure margins and processor relationships.

A chargeback also creates more drag than a routine ACH return. You may lose the sale, pay a fee, and spend staff time answering the dispute. By contrast, most ACH returns are about fixing the payment setup or collecting a new authorization.

Recurring billing creates repeat chances for both problems. A bank debit can fail because payday hasn’t hit yet. Meanwhile, a cardholder can forget they signed up months ago and file a dispute on renewal day. The revenue loss may look similar in your dashboard, but the right next step is very different.

The real difference between ACH returns and chargebacks

Once you separate the payment rails, the decisions get clearer. ACH returns follow bank-transfer rules and NACHA thresholds. Chargebacks follow card-network dispute rules, evidence standards, and strict response windows.

This quick comparison puts the split into plain view:

| Area | ACH return | Card chargeback |

|---|---|---|

| Payment rail | Bank account debit | Credit or debit card |

| Who starts it | Receiving bank returns the entry | Issuing bank opens a dispute |

| Common triggers | NSF, closed account, bad details, revoked authorization | Fraud claim, unclear renewal, service complaint |

| Code style | Return codes such as R01 or R10 | Network reason codes |

| Typical next step | Retry, update details, or get new consent | Refund fast or fight with evidence |

| Main risk | Return-rate limits | Fees, lost revenue, dispute ratio |

NACHA limits matter here. Overall ACH returns must stay under 15%, administrative returns under 3%, and unauthorized returns under 0.5% across the review window. Actual network averages are far lower, so a rising return rate should worry you well before you hit the cap.

The biggest operational difference is control. With ACH, the code tells you what to do next. Retry an R01 carefully, fix data on an R03, and stop rebilling until you get fresh permission after an unauthorized return. With cards, time matters more. If you catch an alert early in the chargeback lifecycle, a refund may stop the dispute before it becomes a formal chargeback.

Some processors also blur the terms and refer to unauthorized ACH cases as “ACH chargebacks.” Forte’s ACH dispute explainer makes clear that these cases still run through ACH return rules, not the normal Visa or Mastercard dispute process.

How subscription merchants should reduce both

Good prevention starts before the payment fails. For ACH, that means clean bank data, clear authorization language, renewal reminders, and smart retry logic for insufficient funds. It also helps to keep dunning respectful and simple, because you want a saved payment, not a canceled customer. Guidance on ACH payments for subscriptions points to the same pattern, fewer bad debits and less involuntary churn.

Card disputes need a different defense. Customers should recognize your descriptor, find cancellation in a few clicks, and reach support before they call the bank. You also need to know the difference between refunds and chargebacks, because a timely refund often costs less than a formal dispute. If card disputes keep climbing, chargeback monitoring programs stop being a theory and become an expensive problem.

Operations matter here, too. Teams do better when ACH exceptions and card disputes go to separate queues. One queue handles retries, account updates, and fresh authorization. The other handles alerts, refunds, and card-network deadlines.

Chargebase fits that second queue. It is chargeback prevention software for e-commerce and SaaS teams that want to cut the number of disputes before they turn into chargebacks. The platform connects to a payment provider with no code, often in about two minutes, then uses networks and programs such as Ethoca, CDRN, and Verifi RDR to surface real-time alerts when a refund can still prevent the case. Merchants can set more than 10 automation rules, choose manual or automatic refund paths where the network allows it, and pay on a per-alert basis. For most companies that accept cards, that mix of alerts and automation lowers the number of chargebacks without adding more manual work.

Conclusion

Treat ACH return codes as signals about a bank debit, and treat chargebacks as formal card disputes. When those workflows get mixed together, teams retry the wrong payments, miss dispute windows, and lose revenue they could have kept.

Recurring billing will always create some payment friction. Still, clean authorization, better renewal communication, and early dispute prevention keep that friction from turning into avoidable losses.

You might also want to read

Uncategorized

Jun 07, 2026

Uncategorized

Jun 06, 2026

Manual vs. Automated Processes

Jun 05, 2026

Uncategorized

Jun 04, 2026